ECB-RESTRICTED (until PUBLIC)

Guidance to banks on

non-performing loans

March 2017

Guidance to banks on non-performing loans

1

Contents

1 Introduction 4

1.1 Context of this guidance 4

1.2 Applicability of this guidance 5

1.3 Scope of this guidance 6

1.4 Structure 7

2 NPL strategy 8

2.1 Purpose and overview 8

2.2 Assessing the operating environment 8

2.3 Developing the NPL strategy 12

2.4 Implementing the operational plan 15

2.5 Embedding the NPL strategy 16

2.6 Supervisory reporting 17

3 NPL governance and operations 18

3.1 Purpose and overview 18

3.2 Steering and decision making 18

3.3 NPL operating model 19

3.4 Control framework 27

3.5 Monitoring of NPLs and NPL workout activities 29

3.6 Early warning mechanisms/watch-lists 35

3.7 Supervisory reporting 38

4 Forbearance 39

4.1 Purpose and overview 39

4.2 Forbearance options and their viability 39

4.3 Sound forbearance processes 44

4.4 Affordability assessments 45

4.5 Supervisory reporting and public disclosures 46

Guidance to banks on non-performing loans

2

5 NPL recognition 47

5.1 Purpose and overview 47

5.2 Implementation of the NPE definition 49

5.3 Link between NPEs and forbearance 54

5.4 Further aspects of the non-performing definition 59

5.5 Links between regulatory and accounting definitions 61

5.6 Supervisory reporting and public disclosures 63

6 NPL impairment measurement and write-offs 65

6.1 Purpose and overview 65

6.2 Individual estimation of provisions 67

6.3 Collective estimation of provisions 74

6.4 Other aspects related to NPL impairment measurement 78

6.5 NPL write-offs 79

6.6 Timeliness of provisioning and write-off 81

6.7 Provisioning and write-off procedures 82

6.8 Supervisory reporting and public disclosures 85

7 Collateral valuation for immovable property 86

7.1 Purpose and overview 86

7.2 Governance, procedures and controls 87

7.3 Frequency of valuations 90

7.4 Valuation methodology 91

7.5 Valuation of foreclosed assets 95

7.6 Supervisory reporting and public disclosures 97

Annex 1 Glossary 98

Annex 2 Sample of NPL segmentation criteria in retail 101

Annex 3 Benchmark for NPL monitoring metrics 104

Annex 4 Samples of early warning indicators 106

Annex 5 Common NPL-related policies 108

ECB-RESTRICTED (until PUBLIC)

Guidance to banks on non-performing loans − Introduction

4

1 Introduction

1.1 Context of this guidance

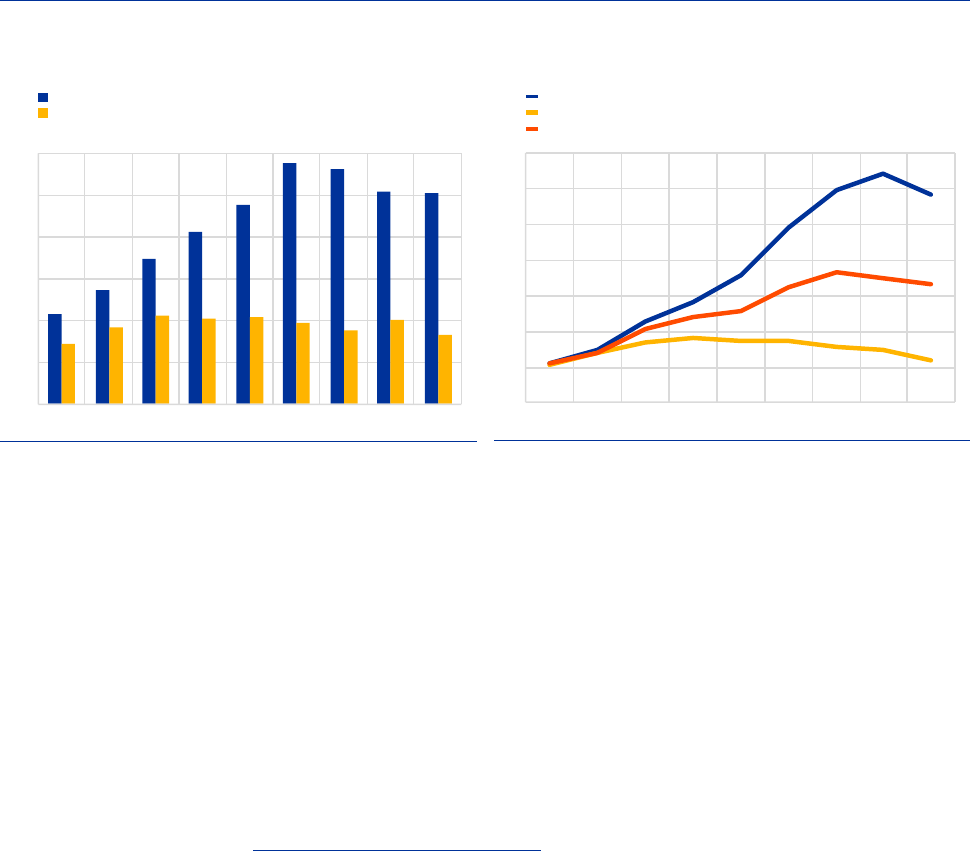

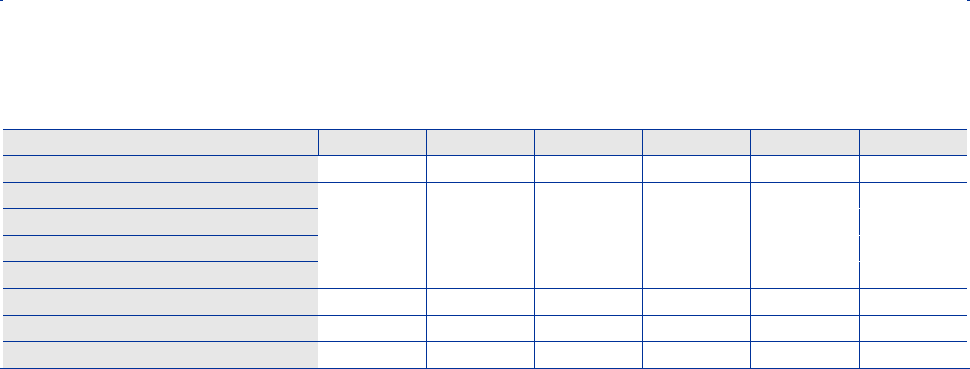

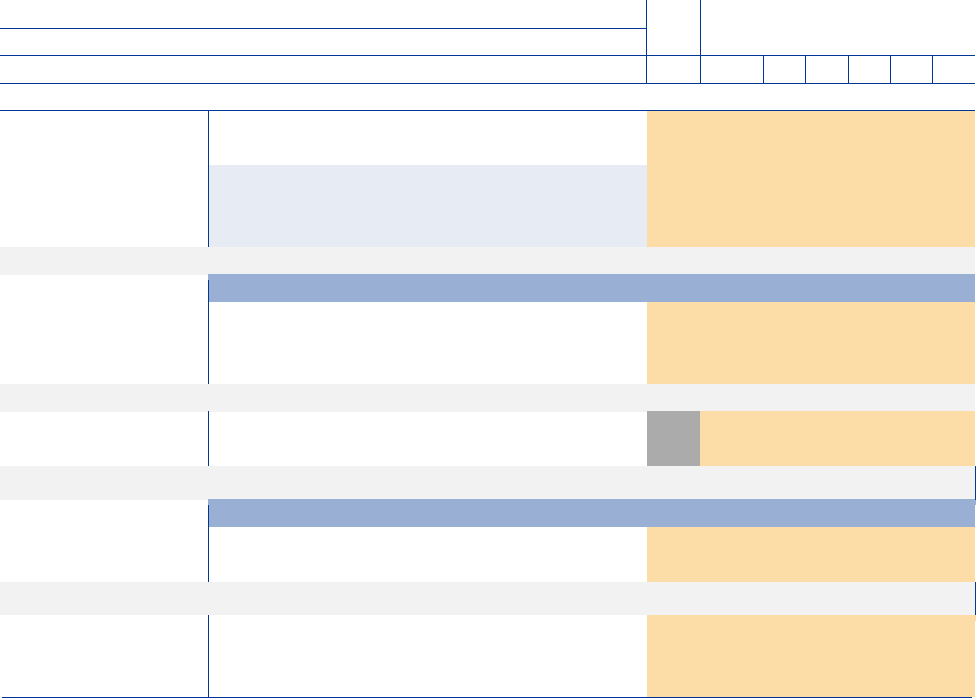

A number of banks in Member States across the Euro area are currently

experiencing high levels of non-performing loans (NPLs), as shown in Figure 1.

There is broad consensus on the view that high NPL levels ultimately have a

negative impact on bank lending to the economy

1

, as a result of the balance sheet,

profitability, and capital constraints faced by banks with high NPL levels.

Figure 1

Texas ratio and Impaired loan ratio evolution in the euro area

Impaired loan ratios for euro area significant banking groups

(2007-2015; percentage of loans, median values)

Source: SNL Financial.

Notes: Based on publicly available data for a sample of 55 significant banking groups.

Countries most affected by the crisis include Cyprus, Greece, Ireland, Italy, Portugal,

Slovenia and Spain.

The deliberate and sustainable reduction of NPLs in banks’ balance sheets is

beneficial to the economy from both a microprudential and a macroprudential

perspective. At the same time, it is acknowledged that economic recovery is also an

important enabler of NPL resolution.

Addressing asset quality issues is one of the key priorities for European Central

Bank (ECB) banking supervision. The ECB’s focus on this issue began with the 2014

comprehensive assessment, which comprised two main pillars – an asset quality

review and a stress test. Subsequent to the comprehensive assessment, ECB

banking supervision continued to intensify its supervisory work on NPLs. In the

context of on-going supervisory engagement, the joint supervisory teams (JSTs)

1

See ECB and other international research, e.g. International Monetary Fund (IMF) discussion note

“Strategy for Resolving Europe’s Problem Loans”

0

2

4

6

8

10

12

14

20 07 20 08 20 09 20 10 20 11 20 12 20 13 20 14 20 15

countr ies most affected by the financial crisis

other countr ies

all countr ies

Ratio of non-performing loans to tangible equity and loan

loss reserves for euro area significant banking groups

(2007-2015; percentages; median values)

Source: SNL Financial.

Notes: Based on publicly available data for a sample of significant banking groups.

Countries most affected by the financial crisis are Cyprus, Greece, Ireland, Italy,

Portugal, Slovenia and Spain.

0

20

40

60

80

10 0

12 0

20 07 20 08 20 09 20 10 20 11 20 12 20 13 20 14 20 15

countr ies most affected by the financial crisis

other countr ies

Guidance to banks on non-performing loans − Introduction

5

have observed varying approaches by banks to the identification, measurement,

management and write-off of NPLs. In this regard, in July 2015 a high-level group on

non-performing loans (comprising staff from the ECB and national competent

authorities) was mandated by the Supervisory Board of the ECB to develop a

consistent supervisory approach to NPLs.

Furthermore, in its supervisory priorities, ECB banking supervision has highlighted

credit risk and heightened levels of non-performing loans as key risks facing euro

area banks.

Through the work of the high-level group, ECB banking supervision has identified a

number of best practices that it deems useful to set out in this public guidance

document. These practices are intended to constitute ECB banking

supervision's supervisory expectation from now on.

This guidance contains predominantly qualitative elements. The intention is to

extend the scope of the guidance based on the continuous monitoring of

developments concerning NPLs. As a next step in this regard, the ECB plans to

place a stronger focus on enhancing the timeliness of provisions and write-offs.

While it is acknowledged that addressing non-performing loans will take some time

and will require a medium-term focus, the principles identified will also serve as a

basic framework for conducting the supervisory evaluation of banks in this specific

area. As part of their ongoing supervisory work, the JSTs will engage with banks

regarding the implementation of this guidance. It is expected that banks will apply the

guidance proportionately and with appropriate urgency, in line with the scale and

severity of the NPL challenges they face.

1.2 Applicability of this guidance

This guidance is addressed to credit institutions within the meaning of Article 4(1) of

Regulation (EU) 575/2013 (CRR)

2

, hereinafter named “banks”. It is generally

applicable to all significant institutions (SIs) supervised directly under the Single

Supervisory Mechanism (SSM), including their international subsidiaries. However,

the principles of proportionality and materiality apply. Hence, parts of this document,

namely chapters 2 and 3 on NPL strategy, governance and operations, may be more

relevant for banks with high levels of NPLs (“high NPL banks”) that need to deal with

this extraordinary situation. Nonetheless, SIs with a relatively low overall level of

NPLs might still find it useful to apply certain parts of those chapters, e.g. to high

NPL portfolios. Chapters 4, 5, 6 and 7 are considered applicable to all SIs.

For the purpose of this guidance, the ECB’s banking supervision defines high NPL

banks as banks with an NPL level that is considerably higher than the EU average

2

Regulation (EU) No 575/2013 of the European Parliament and of the Council of 26 June 2013 on

prudential requirements for credit institutions and investment firms and amending Regulation (EU)

No 648/2012 (OJ L 176, 27.6.2013, p. 1).

Guidance to banks on non-performing loans − Introduction

6

level.

3

However, this definition is highly simplified and banks not falling under its

terms might still benefit from applying the full content at their own initiative or on

request by supervisors, especially in the case of significant NPL inflows, high levels

of forbearance or foreclosed assets, low provision coverage or an elevated Texas

ratio

4

.

This NPL guidance is currently non-binding in nature. However, banks should

explain and substantiate any deviations upon supervisory request. This guidance is

taken into consideration in the SSM regular Supervisory Review and Evaluation

Process and non-compliance may trigger supervisory measures.

This guidance does not intend to substitute or supersede any applicable regulatory

or accounting requirement or guidance from existing EU regulations or directives and

their national transpositions or equivalent, or guidelines issued by the European

Banking Authority (EBA). Instead, the guidance is a supervisory tool with the aim of

clarifying the supervisory expectations regarding NPL identification, management,

measurement and write-offs in areas where existing regulations, directives or

guidelines are silent or lack specificity. Where binding laws, accounting rules and

national regulations on the same topic exist, banks should comply with those. It is

also expected that banks do not enlarge already existing deviations between

regulatory and accounting views in the light of this guidance, but rather the opposite:

whenever possible, banks should foster a timely convergence of regulatory and

accounting views where those differ substantially.

This guidance should be applicable as of its date of publication. SIs may, however,

close identified gaps thereafter based on suitable time-bound action plans which

should be agreed with their respective JSTs. In order to ensure consistency and

comparability, the expected enhanced disclosures on NPLs should start from 2018

reference dates.

1.3 Scope of this guidance

“NPLs” is generally used in this guidance as a shorthand term. However, in technical

terms, the guidance addresses all non-performing exposures (NPEs), following the

EBA definition

5

, as well as foreclosed assets, and also touches on performing

exposures with an elevated risk of turning non-performing, such as “watch-list”

exposures and performing forborne exposures. “NPL” and “NPE”’ are used

interchangeably within this guidance.

3

A suitable reference to determine EU average NPL ratios and coverage levels is the quarterly

published European Banking Authority (EBA) risk dashboard.

4

Definitions of different concepts used in this Guidance can be found in the Glossary in Annex 1.

5

See chapter 5 for details.

Guidance to banks on non-performing loans − Introduction

7

1.4 Structure

The document structure follows the life cycle of NPL management. It starts with the

supervisory expectations on NPL strategies in chapter 2, which closely link to NPL

governance and operations, covered in chapter 3. Following this, the guidance

outlines important aspects for forbearance treatments, in chapter 4, and NPL

recognition, in chapter 5. Qualitative guidance on NPL provisioning and write-off is

treated in chapter 6 while collateral valuations are addressed in chapter 7.

Guidance to banks on non-performing loans − NPL strategy

8

2 NPL strategy

2.1 Purpose and overview

An NPL strategy establishes strategic objectives for high NPL banks for the time-

bound reduction of NPLs over realistic but sufficiently ambitious time-bound horizons

(NPL reduction targets). It should lay out the bank’s approach and objectives

regarding the effective management (i.e. maximisation of recoveries) and ultimate

reduction of NPL stocks in a clear, credible and feasible manner for each relevant

portfolio.

The following steps are considered to be the core building blocks related to the

development and implementation of an NPL strategy:

1. assessing the operating environment, including internal NPL capabilities,

external conditions impacting NPL workout and capital implications (see section

2.2);

2. developing the NPL strategy, including targets in terms of development of

operational capabilities (qualitative) and projected NPL reductions (quantitative)

over the short, medium and long-term time horizons (see section 2.3);

3. implementing the operational plan, including any necessary changes in the

organisational structure of the bank (see section 2.4);

4. fully embedding NPL strategy into the management processes of the bank, also

including a regular review and independent monitoring (see section 2.5).

Governance aspects relating to the NPL strategy are mostly covered in chapter 3.

2.2 Assessing the operating environment

Understanding the full context of the operating environment, both internally and

externally, is fundamental to developing an ambitious yet realistic NPL strategy.

The first phase in the formulation and execution of a fit-for-purpose NPL strategy is

for the bank to complete an assessment of the following elements:

1. the internal capabilities to effectively manage, i.e. maximise recoveries, and

reduce NPLs over a defined time horizon;

2. the external conditions and operating environment;

3. the capital implications of the NPL strategy.

Guidance to banks on non-performing loans − NPL strategy

9

2.2.1 Internal capabilities/self-assessment

There are a number of key internal aspects that influence the bank’s need and ability

to optimise its management of, and thus reduce, NPLs and foreclosed assets (where

relevant). A thorough and realistic self-assessment should be performed to

determine the severity of the situation and the steps that need to be taken internally

to address it.

The bank should fully understand and examine:

• Scale and drivers of the NPL issue:

• the size and evolution of its NPL portfolios on an appropriate level of

granularity, which requires appropriate portfolio segmentation as outlined

in chapter 3;

• the drivers of NPL in-flows and out-flows, by portfolio where relevant;

• other potential correlations and causations.

• Outcomes of NPL actions taken in the past:

• types and nature of actions implemented, including forbearance measures;

• the success of the implementation of those activities and related drivers,

including the effectiveness of forbearance treatments.

• Operational capacities (processes, tools, data quality, IT/automation,

staff/expertise, decision making, internal policies, and any other relevant area

for the implementation of the strategy) for the different process steps involved,

including but not limited to:

• early warning and detection/recognition of NPLs;

• forbearance;

• provisioning;

• collateral valuations;

• recovery/legal process/foreclosure;

• management of foreclosed assets (if relevant);

• reporting and monitoring of NPLs and effectiveness of NPL workout

solutions.

For each of the process steps involved, including those listed above, banks should

perform a thorough self-assessment to determine strengths, significant gaps and any

areas of improvement required for them to reach their NPL reduction targets. The

resulting internal report should be shared with the management body and

supervisory teams.

Guidance to banks on non-performing loans − NPL strategy

10

Banks should repeat or update relevant aspects of the self-assessment at least

annually and also regularly seek independent expert views on these aspects if

necessary.

2.2.2 External conditions and operational environment

Understanding the current and possible future external operating

conditions/environment is fundamental to the establishment of an NPL strategy and

associated NPL reduction targets. Related developments should be closely followed

by banks, which should update their NPL strategies as needed. The following list of

external factors should be taken into account by banks when setting their strategy. It

should not be seen as exhaustive as other factors not listed below might play an

important role in specific countries or circumstances.

Macroeconomic conditions

Macroeconomic conditions will play a key role in setting the NPL strategy and are

best incorporated in a dynamic manner. This also includes the dynamics of the real

estate market

6

and its specific relevant sub-segments. For banks with specific sector

concentrations in their NPL portfolios (e.g. shipping or agriculture), a thorough and

constant analysis of the sector dynamics should be performed, to inform the NPL

strategy.

A reduction of the risk stemming from NPLs can be achieved and should be the aim,

even in less favourable macroeconomic conditions.

7

Market expectations

Assessing the expectations of external stakeholders (including but not limited to

rating agencies, market analysts, research, and clients) with regard to acceptable

NPL levels and coverage will help to determine how far and how fast high NPL

banks should reduce their portfolios. These stakeholders will often use national or

international benchmarks and peer analysis.

NPL investor demand

Trends and dynamics of the domestic and international NPL market for portfolio

sales will help banks make informed strategic decisions regarding projections on the

likelihood and possible pricing of portfolio sales. However, investors ultimately price

6

Unless exposures secured by real estate collateral are not relevant within the NPL portfolios.

7

An example of the target framework applied by Greek significant institutions is provided later in this

chapter.

Guidance to banks on non-performing loans − NPL strategy

11

on a case-by-case basis and one of the determinants of pricing is the quality of

documentation and exposure data that banks can provide on their NPL portfolios.

NPL servicing

Another factor that might influence the NPL strategy is the maturity of the NPL

servicing industry. Specialised servicers can significantly reduce NPL maintenance

and workout costs. However, such servicing agreements need to be well steered and

well managed by the bank.

Regulatory, legal and judicial framework

National as well as European and international regulatory, legal and judicial

frameworks influence the banks’ NPL strategy and their ability to reduce NPLs. For

example, legal or judicial impediments to collateral enforcement influence a bank’s

ability to commence legal proceedings against borrowers or to receive assets in

payment of debt and will also affect collateral execution costs in loan loss

provisioning estimations. Therefore, banks should have a good understanding of the

particularities of legal proceedings linked to the NPL workout for different classes of

assets and also in the different jurisdictions in which they operate where high levels

of NPLs are present. In particular, they should assess: the average length of such

proceedings, the average financial outcomes, the rank of different types of

exposures and related implications for the outcome (for instance regarding secured

and unsecured exposures), the influence of the types and ranks of collateral and

guarantees on the outcomes (for instance related to second or third liens and

personal guarantees), the impact of consumer protection issues on legal decisions

(especially for retail mortgage exposures), and the average total costs associated

with legal proceedings. Furthermore, the consumer protection legal environment

should also be borne in mind as it also plays a role in client communication and

interaction.

Tax implications

National tax implications of provisioning and NPL write-offs will also influence NPL

Strategies.

2.2.3 Capital implications of the NPL strategy

Capital levels and their projected trends are important inputs to determining the

scope of NPL reduction actions available to banks. Banks should be able to

dynamically model the capital implications of the different elements to their NPL

strategy, ideally under different economic scenarios. Those implications should also

Guidance to banks on non-performing loans − NPL strategy

12

be considered in conjunction with the risk appetite framework (RAF) as well as the

internal capital adequacy assessment process (ICAAP).

Where capital buffers are slim and profitability low, high NPL banks should include

suitable actions in their capital planning which will enable a sustainable clean-up of

NPLs from the balance sheet.

2.3 Developing the NPL strategy

An NPL strategy should encompass, at a minimum, time-bound quantitative NPL

targets supported by a corresponding comprehensive operational plan. It should be

based on a self-assessment and an analysis of NPL strategy implementation

options. The NPL strategy, including the operational plan, should be approved by the

management body and reviewed at least annually.

2.3.1 Strategy implementation options

On the basis of the above-described assessment, banks should review the range of

NPL strategy implementation options available and their respective financial impact.

Examples of implementation options, not being mutually exclusive, are:

• Hold/forbearance strategy: A hold strategy option is strongly linked to operating

model, forbearance and borrower assessment expertise, operational NPL

management capabilities, outsourcing of servicing and write-off policies.

• Active portfolio reductions: These can be achieved either through sales and/or

writing off provisioned NPL exposures that are deemed unrecoverable. This

option is strongly linked to provision adequacy, collateral valuations, quality

exposure data and NPL investor demand.

• Change of exposure type: This includes foreclosure, debt to equity swapping,

debt to asset swapping, or collateral substitution.

• Legal options: This includes insolvency proceedings or out-of-court solutions.

Banks should ensure that their NPL strategy includes not just a single strategic

option but rather combinations of strategies/options to best achieve their objectives

over the short, medium and long term and explore which options are advantageous

for different portfolios or segments (see section 3.3.2 regarding portfolio

segmentation) and under different conditions.

Banks should also identify medium and long-term strategy options for NPL

reductions which might not be achievable immediately, e.g. a lack of immediate NPL

investor demand might change in the medium to long term. Operational plans might

need to foresee such changes, e.g. the need for enhancing the quality of NPL

exposure data in order to be ready for future investor transactions.

Guidance to banks on non-performing loans − NPL strategy

13

Where banks assess that the above-listed implementation options do not provide an

efficient NPL reduction in the medium to long-term horizon for certain portfolios,

segments or individual exposures, this should be clearly reflected in an appropriate

and timely provisioning approach. The bank should write off loans which are deemed

to be uncollectable in a timely manner.

Finally, it is acknowledged that NPL risk transfer and securitisation transactions can

be beneficial for banks in terms of funding, liquidity management, specialisation and

efficiency. However, these are usually complex processes and should be conducted

with care. Consequently, institutions wanting to engage in such transactions are

expected to conduct robust risk analysis and to have adequate risk control

processes

8

(see Annex 8 for more details).

2.3.2 Targets

Before commencing the short to medium-term target-setting process, banks should

establish a clear view of what reasonable long-term NPL levels are, both on an

overall basis but also on a portfolio-level basis. It is acknowledged that there is a

considerable amount of uncertainty around the timeframes required to achieve these

long-term goals, but they are an important input to setting adequate short and

medium-term targets. Banks working in tense macroeconomic conditions should also

explore international or historic benchmarks in order to define “reasonable” long-term

NPL levels.

9

High NPL banks should include, at a minimum, clearly defined quantitative targets in

their NPL strategy (where relevant including foreclosed assets), which should be

approved by the management body. The combination of these targets should lead to

a concrete reduction, gross and net (of provisions), of NPL exposures, at least in the

medium term. While expectations about changes in macroeconomic conditions can

play a role in determining target levels (if based on solid external forecasts), they

should not be the sole driver for the established NPL reduction targets.

Targets should be established at least along the following dimensions:

• by time horizons, i.e. short-term (indicative 1 year), medium-term (indicative 3

years) and possibly long-term;

• by main portfolios (e.g. retail mortgage, retail consumer, retail small businesses

and professionals, SME corporate, large corporate, commercial real estate);

• by implementation option chosen to drive the projected reduction, e.g. cash

recoveries from hold strategy, collateral repossessions, recoveries from legal

proceedings, revenues from sale of NPLs or write-offs.

8

As required for securitisations under Article 82(1) CRD.

9

For short to medium-term targets international benchmarks are less relevant.

Guidance to banks on non-performing loans − NPL strategy

14

For high NPL banks, the NPL targets should at a minimum include a projected

absolute or percentage NPL exposure reduction, both gross and net of provisions,

not only on an overall basis but also for the main NPL portfolios. Where foreclosed

assets are material

10

, a dedicated foreclosed assets strategy should be defined or, at

least, foreclosed assets reduction targets should be included in the NPL strategy. It

is acknowledged that a reduction in NPEs might involve an increase in foreclosed

assets for the short term, pending the sale of these assets. However, this timeframe

should be clearly limited as the aim of foreclosures is a timely sale of the assets

concerned. The supervisory expectation for the valuation and approach to foreclosed

assets is included in section 7.5. This should be reflected in the NPL strategy.

The targets described should be aligned with more granular operational targets. Any

of the monitoring indicators discussed in detail in section 3.5.3 can be implemented

as an additional target if deemed appropriate, e.g. related to NPL flows, coverage,

cash recoveries, the quality of forbearance measures (e.g. redefault rates), the

status of legal actions or the identification of non-viable (denounced) exposures. It

should be ensured that such additional NPL targets have an appropriate focus on

high risk exposures, e.g. legal cases or late arrears.

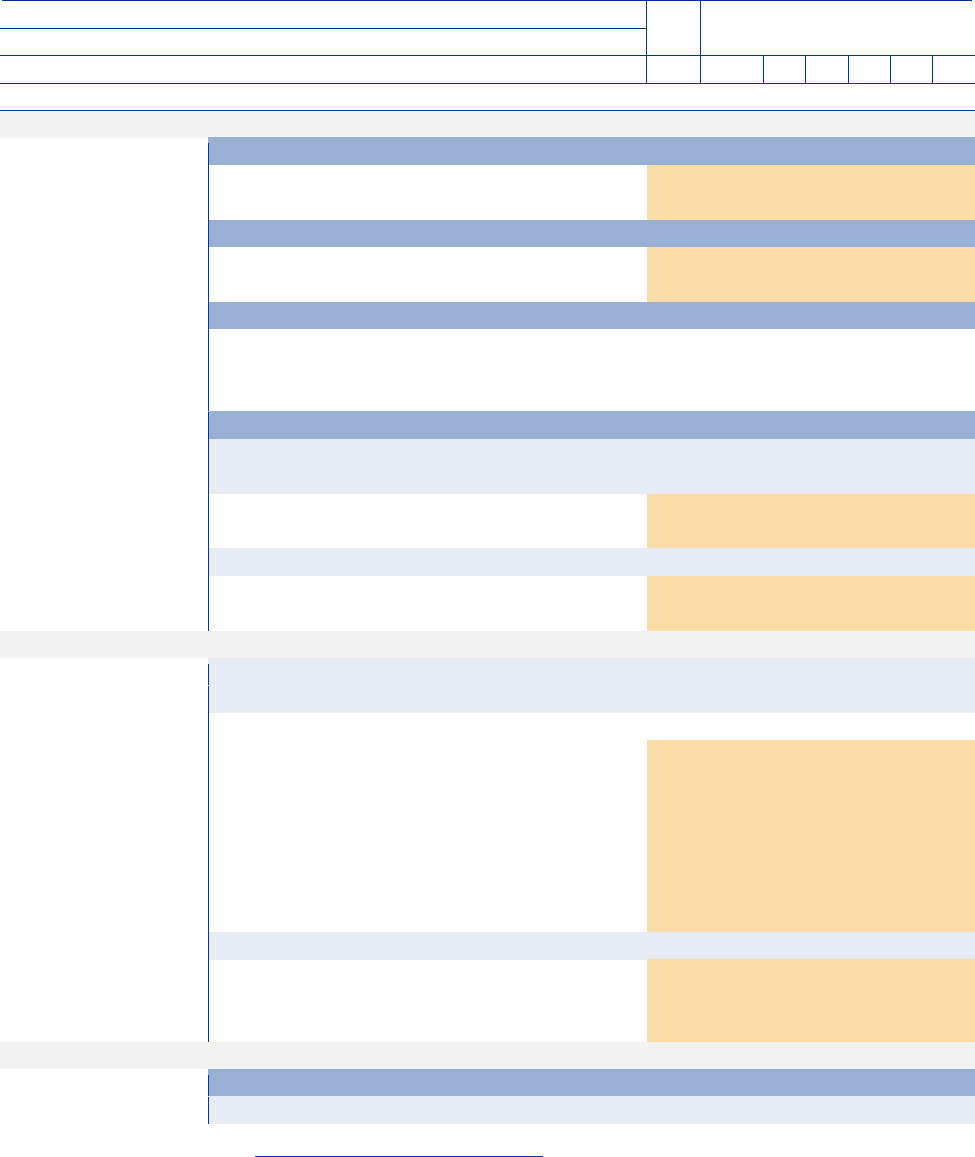

Example 1 shows high-level quantitative targets which have been implemented by

Greek significant institutions in 2016. Targets were initially defined for all main

portfolios on a quarterly basis for the first year. Each of these high-level targets was

also accompanied by a standard set of more granular monitoring items, e.g. NPE

ratio and coverage ratio for Target 1 or a breakdown of sources of collections for

Target 3.

Example 1

Example of high-level NPL targets implemented by Greek SIs in 2016

Result-oriented operational targets

1 NPE Volume (Gross)

2 NPL Volume (Gross)

3 Cash recoveries (collections, liquidations and sales) from NPEs / Total average NPEs

Sustainable solutions-oriented operational target

4 Loans with long term modifications / NPE plus Performing forborne exposures with Long Term Modifications

Action-oriented operational targets

5 NPE >720 dpd not denounced / (NPE >720 dpd not denounced + denounced)

6 Denounced loans for which legal action has been initiated / Total denounced loans

7 Active NPE SMEs

11

for which a viability analysis has been conducted in the last 12 months / Active NPE SMEs

8 SME and Corporate NPE common borrowers

12

for which a common restructuring solution has been implemented

9 Corporate NPE for which the bank(s) have engaged a specialist for the implementation of a company restructuring plan

10

For example if the ratio of foreclosed assets over total loans plus foreclosed assets is significantly

above the average for EU banks having the option to foreclose assets.

11

A company/ business is considered as “active” when it is not “idle”. The term “idle business” is based

on Greek law and refers to businesses with no activity during the reference period.

12

“Common” refers to debtors that have exposures with more than one bank.

Guidance to banks on non-performing loans − NPL strategy

15

Banks running the NPL strategy process for the first time will likely have a stronger

focus on qualitative targets for the short-term horizon. The aim here is to address the

deficiencies identified during the self-assessment process and thus establish an

effective and timely NPL management framework which allows the successful

implementation of the quantitative NPL targets approved for the medium to long-term

horizon.

2.3.3 Operational plan

The NPL strategy of a high NPL bank should be supported by an operational plan

which is also approved by the management body. The operational plan should

clearly define how the bank will operationally implement its NPL strategy over a time

horizon of at least 1 to 3 years (depending on the type of operational measures

required).

The NPL operational plan should contain at a minimum:

• clear time-bound objectives and goals;

• activities to be delivered on a segmented portfolio basis;

• governance arrangements including responsibilities and reporting mechanisms

for defined activities and outcomes;

• quality standards to ensure successful outcomes;

• staffing and resource requirements;

• required technical infrastructure enhancement plan;

• granular and consolidated budget requirements for the implementation of the

NPL strategy;

• interaction and communication plan with internal and external stakeholders (e.g.

for sales, servicing, efficiency initiatives etc.).

The operational plan should put a specific focus on internal factors that could present

impediments to a successful delivery of the NPL strategy.

2.4 Implementing the operational plan

The implementation of the NPL operational plans should rely on suitable policies and

procedures, clear ownership and suitable governance structures (including

escalation procedures).

Any deviations from the plan should be highlighted and reported to the management

body in a timely manner with appropriate remediation actions to be put in place.

Guidance to banks on non-performing loans − NPL strategy

16

Some high NPL banks might need to incorporate wide-ranging change management

measures in order to integrate the NPL workout framework as a key element in the

corporate culture.

2.5 Embedding the NPL strategy

As execution and delivery of the NPL strategy involves and depends on many

different areas within the bank, it should be embedded in processes at all levels of

an organisation, including strategic, tactical and operational.

Information

High NPL banks should put significant emphasis on communicating to all staff the

key components of the NPL strategy in line with the approach taken for the

institutions’ overall strategy and vision. This is especially important if the

implementation of the NPL strategy involves wide-ranging changes to business

procedures.

Ownership, incentives, management goals and performance

monitoring

All banks should clearly define and document the roles, responsibilities and formal

reporting lines for the implementation of the NPL strategy, including the operational

plan.

Staff and management involved in NPL workout activities should be provided with

clear individual (or team) goals and incentives geared towards reaching the targets

agreed in the NPL strategy, including the operational plan. These incentives should

be effective and should not be superseded by other, potentially contrary incentives.

Related remuneration policies and performance monitoring frameworks should take

the NPL targets sufficiently into account.

Business plan and budget

All relevant components of the NPL strategy should be fully aligned with and

integrated into the business plan and budget. This includes, for example, the costs

associated with the implementation of the operational plan (e.g. resources, IT, etc.)

but also potential losses stemming from NPL workout activities. Some banks might

find it useful to establish dedicated NPL loss budgets for the latter to facilitate

internal business control and planning.

Guidance to banks on non-performing loans − NPL strategy

17

Risk control framework and culture

The NPL strategy should be fully embedded in the risk control framework. In that

context, special attention should be paid to:

• ICAAP

13

: All relevant components of the NPL strategy should be fully aligned

with and integrated into the ICAAP. High NPL banks are expected to prepare

the quantitative and qualitative assessment of NPL developments under base

and stressed conditions including the impact on capital planning;

• RAF

14

: RAF and NPL strategy are closely interlinked. In this regard, there

should be clearly defined RAF metrics and limits approved by the management

body which are in alignment with the core elements and targets forming part of

the NPL strategy;

• Recovery plan

15

: Where NPL-related indicator levels and actions form part of

the recovery plan, banks should ensure they are in alignment with the NPL

strategy targets and operational plan.

A strong level of monitoring and oversight by risk control functions in respect of the

formulation and implementation of the NPL strategy (including operational plan)

should also be ensured.

2.6 Supervisory reporting

High NPL banks should report their NPL strategy, including the operational plan, to

their Joint Supervisory Teams (JSTs) in the first quarter of each calendar year. To

facilitate comparison, banks should also submit the standard template, as included in

Annex 7 of this guidance, summarising the quantitative targets and the level of

progress made in the past 12 months against plan. This standard template should be

submitted on an annual basis. The management body should approve these

documents prior to submission to supervisory authorities.

For a smooth process, banks should consult with JSTs at an early stage in the NPL

strategy development process.

13

As defined in Article 108 of Directive 2013/36/EU of the European Parliament and of the Council of 26

June 2013, on access to the activity of credit institutions and the prudential supervision of credit

institutions and investment firms (OJ L 176, 27.6.2013, p. 338), known as the CRD; see also Glossary.

14

As described in the Financial Stability Board’s “Principles for An Effective Risk Appetite Framework”;

see also Glossary.

15

As required by Directive 2014/59/EU of the European Parliament and of the Council of 15 May 2014

establishing a framework for the recovery and resolution of credit institutions and investment firms and

amending Council Directive 82/891/EEC, and Directives 2001/24/EC, 2002/47/EC, 2004/25/EC,

2005/56/EC, 2007/36/EC, 2011/35/EU, 2012/30/EU and 2013/36/EU, and Regulations (EU) No

1093/2010 and (EU) No 648/2012, of the European Parliament and of the Council (OJ L 173,

12.6.2014, p. 190), known as the Bank Recovery and Resolution Directive (BRRD) (Directive

2014/59/EU); also see Glossary.

Guidance to banks on non-performing loans − NPL governance and operations

18

3 NPL governance and operations

3.1 Purpose and overview

Without an appropriate governance structure and operational set-up, banks will not

be able to address their NPL issues in an efficient and sustainable way.

This chapter sets out key elements to the governance and operations of an NPL

workout framework starting with key aspects related to steering and decision making

(section 3.2). Following this, it provides guidance with regard to the NPL operating

model (section 3.3), internal control framework and NPL monitoring (sections 3.4 and

3.5) and early warning processes (section 3.6).

3.2 Steering and decision making

In accordance with international and national regulatory guidance, a bank’s

management body should approve and monitor the institution’s strategy.

16

For high

NPL banks, the NPL strategy and operational plan forms a vital part of the

overarching strategy and should therefore be approved and steered by the

management body. In particular, the management body should:

• approve annually and regularly review the NPL strategy including the

operational plan;

• oversee the implementation of the NPL strategy;

• define management objectives (including a sufficient number of quantitative

ones) and incentives for NPL workout activities;

• periodically (at least quarterly) monitor progress made in comparison with the

targets and milestones defined in the NPL strategy, including the operational

plan;

• define adequate approval processes for NPL workout decisions; for certain

large NPL exposures this should involve management body approval;

• approve NPL-related policies and ensure that they are completely understood

by the staff;

• ensure sufficient internal controls over NPL management processes (with a

special focus on activities linked to NPL classifications, provisioning, collateral

valuations and sustainability of forbearance solutions);

16

Also see “SSM supervisory statement on governance and risk appetite” of June 2016

Guidance to banks on non-performing loans − NPL governance and operations

19

• have sufficient expertise with regard to the management of NPLs.

17

The management body and other relevant managers are expected to dedicate an

amount of their capacity to NPL workout-related matters that is proportionate to the

NPL risks within the bank.

Especially as NPL workout volumes pick up, the bank needs to establish and

document clearly defined, efficient and consistent decision-making procedures. In

this context, an adequate second line of defence involvement should be ensured at

all times.

3.3 NPL operating model

3.3.1 NPL workout units

Separate and dedicated units

International experience indicates that a suitable NPL operating model is based on

dedicated NPL workout units (WUs) which are separate from units responsible for

loan origination. Key rationales for this separation are the elimination of potential

conflicts of interest and the use of dedicated NPL expertise from staff through to

management level.

High NPL banks should therefore implement separate and dedicated NPL WUs,

ideally starting from the moment of early arrears

18

but latest by the NPL classification

of an exposure. This separation of duties approach should encompass not only client

relationship activities (e.g. negotiation of forbearance solutions with clients), but also

the decision-making process. In this context, banks should consider implementing

dedicated decision-making bodies related to NPL workout (e.g. NPL committee).

Where overlaps with the bodies, managers or experts involved in the loan origination

process are not avoidable, the institutional framework should ensure that any

potential conflicts of interest are sufficiently mitigated.

It is acknowledged that for some business lines or exposures (e.g. those requiring

special know-how), the implementation of a fully separate organisational unit may

not be possible or may require longer periods to embed. In such cases, internal

controls should ensure a sufficient mitigation of potential conflicts of interest (e.g.

independent view on assessment of borrowers’ creditworthiness).

17

In certain countries banks have started to consciously build up dedicated management body expertise

on NPLs.

18

Where early arrears are not managed separately, there should be adequate policies, controls and IT

infrastructure in place to mitigate the potential conflicts of interest.

Guidance to banks on non-performing loans − NPL governance and operations

20

Though NPL WUs should be separated from loan origination units, a regular

feedback loop between both functions should be established, e.g. to exchange the

information needed for planning NPL inflows or to share lessons learnt from NPL

workouts that are relevant for originating new business.

Alignment with NPL life cycle

NPL WUs should be set-up taking into account the full NPL life cycle

19

to ensure that

NPL workout activities and borrower engagements are tailored, all applicable

workout stages have adequate focus and staff is sufficiently specialised. Relevant

phases in the NPL life cycle are:

• Early arrears (up to 90 days past due (dpd))

20

: During this phase, the focus

is on initial engagement with the borrower for early recoveries and on collecting

information required for a detailed assessment of the borrower’s circumstances

(e.g. financial position, status of loan documentation, status of collateral, level of

cooperation, etc.). The information collection will allow appropriate borrower

segmentation (see section 3.3.2), which ultimately determines the most suitable

workout strategy for the borrower. This phase might also involve short-term

forbearance options (see also chapter 4) with the aim of stabilising the financial

position of the borrower before establishing a suitable workout strategy. In

addition, the bank should seek options to improve its position (for instance by

signing new loan documents, perfecting outstanding security, minimising cash

leakage, taking additional security if available);

• Late arrears / Restructuring / forbearance

21

: This phase is focused on

implementing and formalising restructuring/forbearance arrangements with

borrowers. These restructuring/forbearance arrangements should be put into

place only where the borrower affordability assessment concluded that viable

restructuring options indeed exist (see also chapter 4). Post completion of a

restructuring/forbearance arrangement the borrower should be constantly

monitored for a clearly defined minimum period (recommended to be aligned

with the cure period in the EBA definition of NPE, i.e. at least 1 year), given

their increased risk, before they can eventually be transferred out of the NPL

WUs if no further NPL triggers are observed (see also chapter 5).

• Liquidation / debt recovery / legal cases / foreclosure: This phase focuses

on borrowers for whom no viable forbearance solutions can be found due to the

borrower’s financial circumstances or cooperation level. In such cases, banks

should initially perform a cost-benefit analysis of the different liquidation options

including in-court and out-of-court procedures. Based on this analysis, banks

should speedily proceed with the chosen liquidation option. Dedicated legal and

19

This also encompasses assets not technically classified as NPEs such as early arrears, forborne

exposures or foreclosed assets – which play an essential role in the NPL workout process.

20

Unlikely-to-pay exposures could be part of either early arrears or restructuring units, depending on the

complexity.

21

See footnote 20.

Guidance to banks on non-performing loans − NPL governance and operations

21

business liquidation expertise is crucial for this phase of the NPL life cycle.

Banks that are engaged in extensive use of external experts here should

ensure that sufficient internal control mechanisms are in place to ensure an

effective and efficient liquidation process. Aged NPL stock should be given

special attention in this regard. A dedicated debt recovery policy should contain

guidance on the liquidation procedures (see also Annex 5).

• Management of foreclosed assets (or other assets stemming from NPLs)

High NPL banks should set up different WUs for the different phases of the NPL life

cycle and also for different portfolios if appropriate. It is crucial to implement a clear

formal definition of “hand-over” trigger which describes when an exposure is moved

from the regular/business as usual relationship manager to the NPL WUs and from

the management responsibility of one NPL WU to another. The trigger levels should

be clearly defined and only allow the application of management discretion under

strictly identified circumstances and conditions.

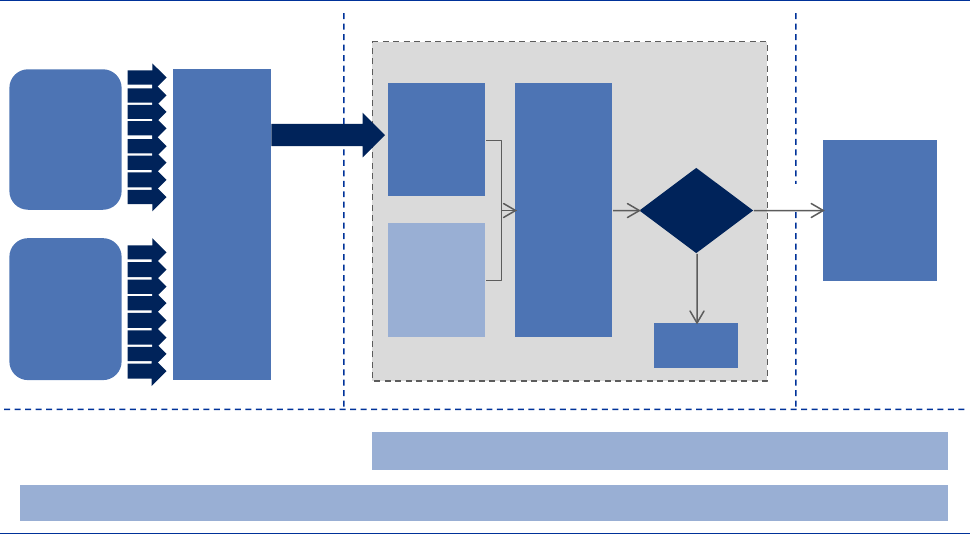

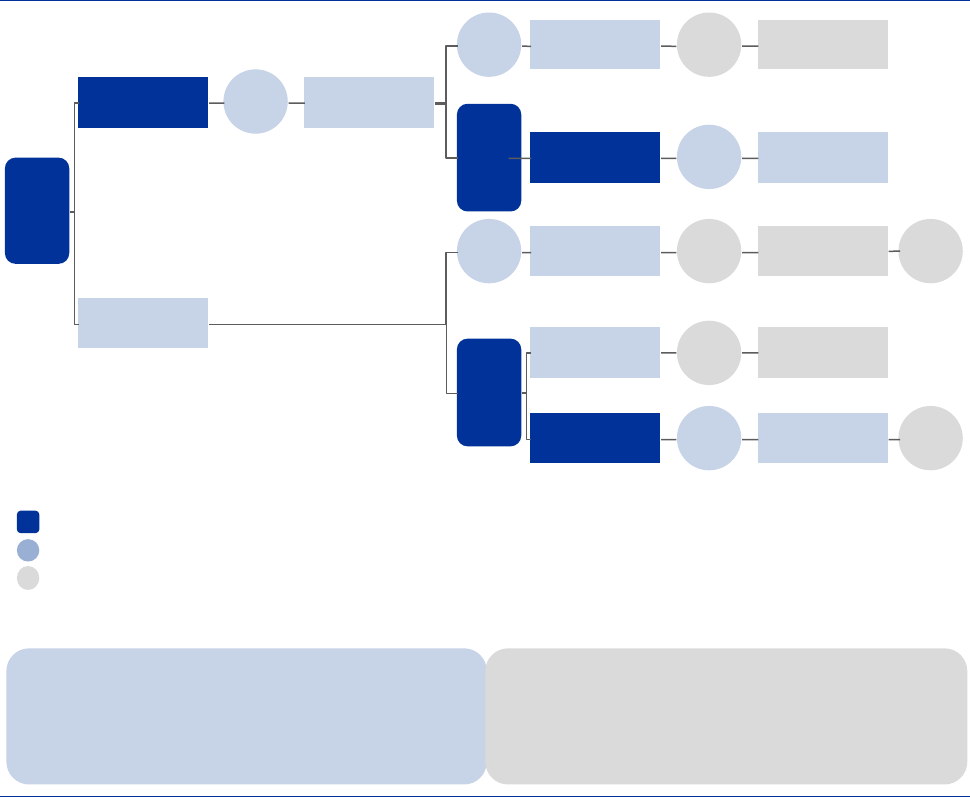

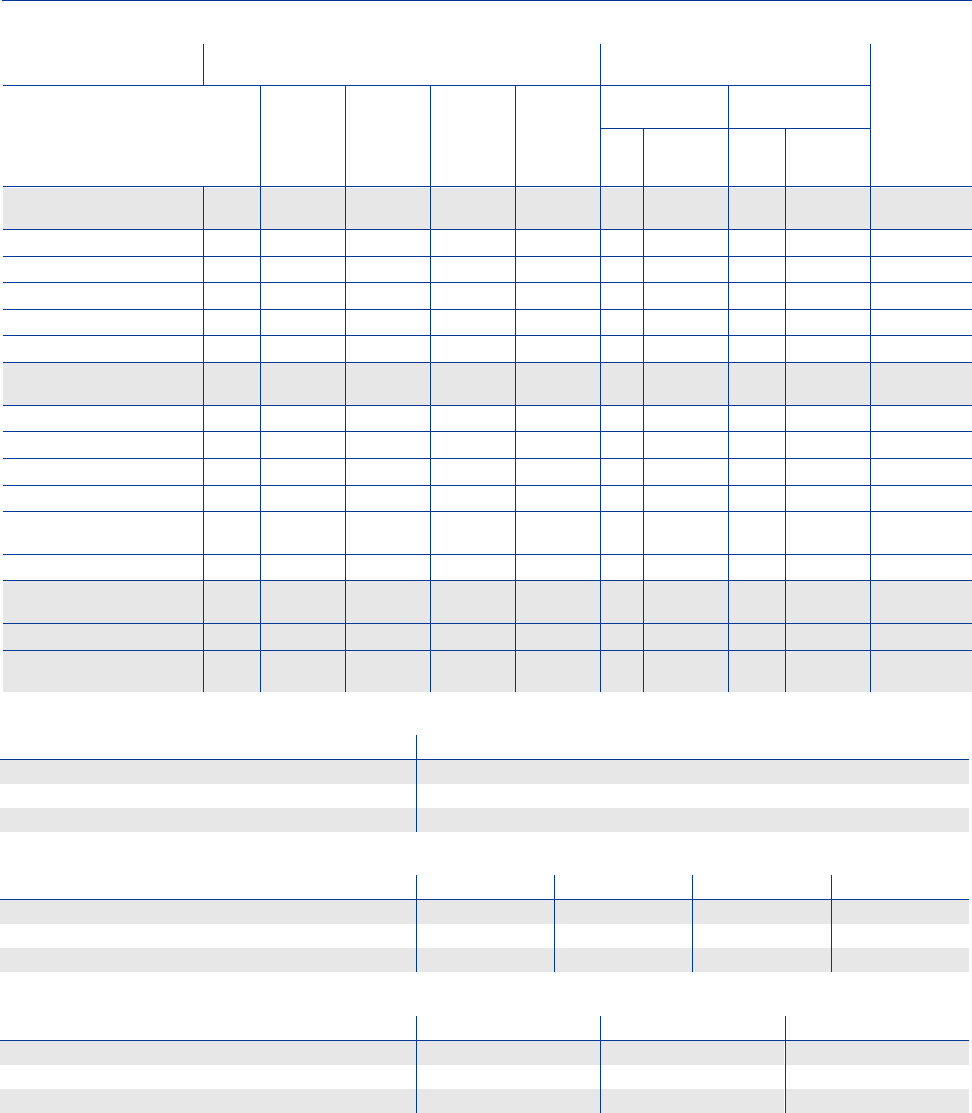

Example 2

Example of an NPL WU structure and triggers implemented by a mid-sized bank

Within the individual NPL WUs, more specialisation is often useful based on the

different NPL workout approaches required per relevant borrower segment (see

section 3.3.2). Monitoring and quality assurance processes should be sufficiently

tailored to these substructures.

A dedicated arrears management policy should contain guidance on the overall NPL

workout procedures and responsibilities, including hand-over triggers (see also

Annex 5).

Relationship

manager

NPL WUs

Retail cus tomers Com mercial customers

• Unsecur ed exposur e

> EUR 50k

• Risk criterion of early warning list

• Placed on risk list

• Exposure > EUR 10 k

• At least 2 remi nders for overdue payment

Restructuring

• Unsecur ed exposur e > EUR 250k and PD scor ing > 13

• Specific pr ovisi on > EUR 250k

• Other e.g . creditors steering meetings

• Complex retail customer exposur es

Liquidation

• Bankruptcy or measure unsuccessful

• Bankruptcy or measure unsuccessful

• Exposures < EUR 100 written off directly

Intensive loan m anagement

Guidance to banks on non-performing loans − NPL governance and operations

22

Example 2 shows an example of an NPL WU structure as implemented by a mid-

sized significant institution, including the triggers applied to determine the

appropriate NPL WU for each borrower. It shows that this bank has assessed it as

being more appropriate to keep early arrears in the commercial portfolio with the

regular market operations/relationship managers while borrowers of all other NPL

exposures are managed by separate and dedicated NPL WUs. Commercial

restructurings and complex retail restructurings are dealt with by the same unit.

Tailoring to portfolio specificities

When designing an appropriate NPL WU structure, banks should take into account

the specificities of their main NPL portfolios as also shown in the example in

Example 2.

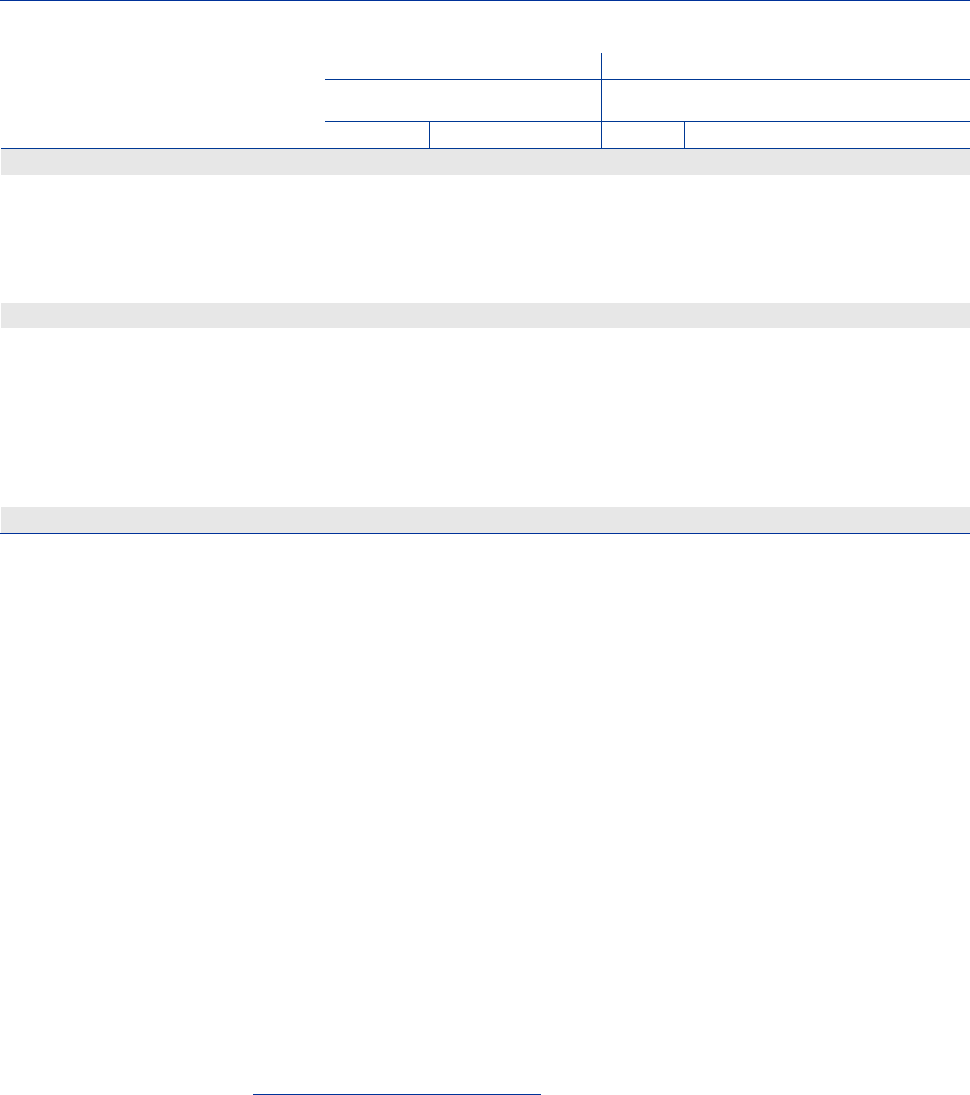

For material retail NPL portfolios a somewhat industrialised process could be

applied, e.g. using a contact centre in the early arrears phase which will be

responsible for the maximisation of early arrears collections (see example in

Example 3). It is important, though, to ensure that even in industrialised approaches

NPL WU staff have access to specialists when required, e.g. for more complex

relationships or products.

Example 3

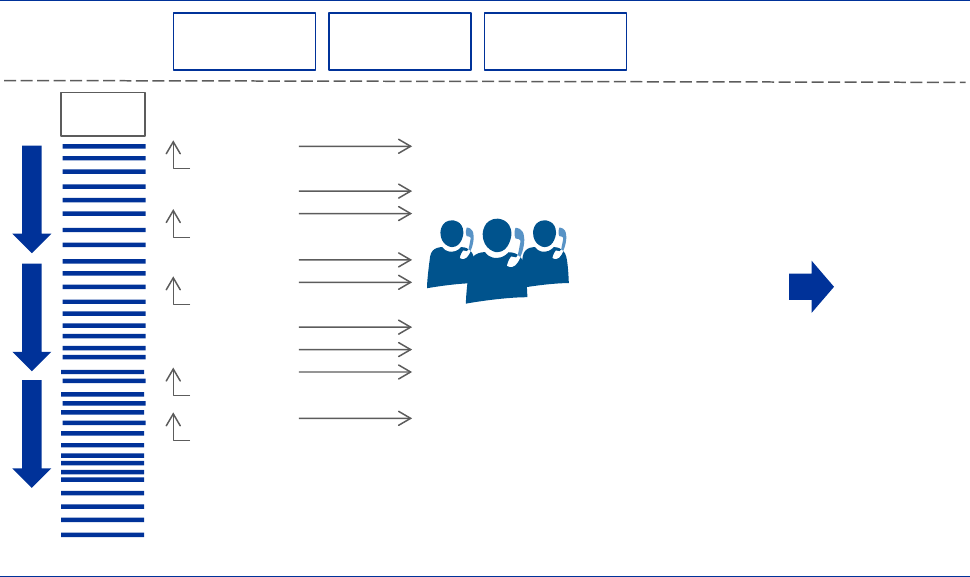

Example of a retail contact centre in the early arrears phase

1-90

Days past due

Restructuring

Team

Outbound

Inbound

In

& Ou t

Available Solutions

• Limited range of solutions

• Cash and promise to pay

• Repayment ag reements

• Options 1-5

• All else to the Restructuring

Team

Dialler List

Connect

No r eply

Connect

Connect

Eng ag ed

Connect

Connect

No r eply

Connect

Connect

Connect

No r eply

Connect

Eng ag ed

Staff Targets

•

Contacts (

RPCs)

• Cash collected

• Promise to pay

• Cur es

• Quality score

Quality Assurance

• All calls recor ded

• Sample of calls scor ed

• 3-7 per agent

• Key qualifier to incentives

Operating Hours

• Mon-Fri = 8am – 9pm

• Sat = 9am – 5pm

• Sun = 10am – 4pm

Dialler Strategy

• High r i sk =

dail y c

all

• Medium r i s k = 2-3 days

• Low r i s k = 5-7 days

Guidance to banks on non-performing loans − NPL governance and operations

23

For corporate NPL portfolios, relationship management rather than industrialised

approaches are usually applied, with a strong sectorial specialisation of NPL WU

staff. For sole traders and micro-SMEs, a combination of industrialised elements and

relationship approaches seems required.

3.3.2 Portfolio segmentation

A suitable operating model is based on analysing the bank’s NPL portfolio with a

high degree of granularity, resulting in clearly defined borrower segments. A

necessary precondition for this analysis (portfolio segmentation) is the development

of appropriate management information (MI) systems and a sufficiently high data

quality.

Portfolio segmentation enables the bank to group borrowers with similar

characteristics requiring similar treatments, e.g. restructuring solutions or liquidation

approaches. Customised processes are then designed for each segment with

dedicated expert teams taking ownership of the segments.

Having regard to the principle of proportionality and the nature of the bank’s portfolio,

segmentation can be conducted by taking multiple borrowers’ characteristics into

consideration. Segmentations should have a useful purpose, meaning that different

segments should generally trigger different treatments by the NPL WUs or dedicated

teams within those units.

For corporate NPL portfolios, for instance, segmentation by asset class or sector is

likely to be a key driver for NPL WU specialisation, i.e. commercial real estate, land

and development, shipping, trading businesses, etc. These portfolios should then be

further segmented by the proposed NPL resolution strategy and the level of financial

difficulties to ensure that the workout activities are sufficiently focused. Borrowers

operating in the same sector will tend to have similar types of credit facilities which

might allow the institution to develop specific restructuring products for the respective

sectorial segments.

A list of potential segmentation criteria for retail NPL portfolios is contained in

Annex 2.

3.3.3 Human resources

Proportionality of the NPL organisation

All banks need to have in place an appropriate and proportionate organisation

relative to their business model and taking into account their risks, including risks

stemming from NPLs. High NPL banks are therefore expected to devote an

appropriate and proportionate amount of management attention and resources to the

workout of those NPLs and to the internal controls of related processes. It should be

Guidance to banks on non-performing loans − NPL governance and operations

24

noted that while there might be some room for sharing management and resources

with other parts of the value chain (e.g. loan origination), such overlaps should be

carefully considered from the points of view of conflicts of interest and sufficient

specialisation as discussed above.

Based on the proportionality criteria and the findings of the bank’s NPL self-

assessment on capabilities, as included in chapter 2, high NPL banks should

regularly review the adequacy of their internal and external NPL workout resources

and regularly determine their capacity needs. As part of this, certain benchmarks

(e.g. workout accounts per full-time equivalent employee) can be set and monitored.

Any staffing gaps arising should be addressed in a speedy fashion. Given the

extraordinary nature of the NPL workout activities, banks might choose to use fixed

term contracts, internal/external outsourcing or joint ventures for NPL workout

activities. In the event that external outsourcing is used, banks should have

dedicated experts to closely control and monitor the effectiveness and efficiency of

the outsourced activities.

22

Expertise and experience

Banks should build up the relevant expertise required for the defined NPL operating

model, including the NPL WUs and control functions. Wherever possible, resources

with dedicated NPL expertise and experience should be hired for key NPL workout

tasks. When this is not possible banks should put an even higher emphasis on

implementing adequate dedicated NPL training and staff development plans to

quickly build in-house expertise using available talent.

23

Where it is not possible or efficient to build in-house expertise and infrastructure, the

NPL WUs should have easy access to qualified independent external resources

(such as property appraisers, legal advisors, business planners, industry experts) or

to those parts of the NPL workout activities which are outsourced to dedicated NPL

servicing companies.

Performance management

For NPL WU staff, individual (if adequate) and team performance should be

monitored and measured on a regular basis. For this purpose, an appraisal system

tailored to the requirements of the NPL WUs should be implemented in alignment

22

Any outsourcing of NPLs should be made in accordance with the general requirements and Guidelines

on the outsourcing of activities by banks of the European Banking Authority (EBA).

23

NPL-related training and development plans should include the following aspects where appropriate:

negotiating skills, dealing with difficult borrowers, guidance on internal NPL policies and procedures,

different forbearance approaches, understanding the local legal framework, obtaining personal and

financial information from clients, conducting borrower affordability assessments (tailored to different

borrower segments) and any other aspect that is relevant to ensure the correct implementation of the

NPL strategy and its operational plans. The major difference in the role and skills required between a

relationship manager role in an NPL WU and a relationship manager role on a performing portfolio

should be reflected in the training framework.

Guidance to banks on non-performing loans − NPL governance and operations

25

with the overall NPL strategy and operational plan. Further to quantitative elements

linked to the bank’s NPL targets and milestones (probably with a strong focus on the

effectiveness of workout activities), the appraisal system may include qualitative

measurements such as level of negotiations competency, technical abilities relating

to the analysis of the financial information and data received, structuring of

proposals, quality of recommendations, or monitoring of restructured cases.

It should also be ensured that the higher degree of commitment (e.g. outside of

regular working hours) usually required of NPL WU staff is sufficiently reflected in the

agreed working conditions, remuneration policies, incentives and performance

management framework.

The performance measurement framework for high NPL banks’ management bodies

and relevant managers should include specific indicators linked to the targets

defined in the NPL strategy and operational plan. The importance of the respective

weight given to these indicators within the overall performance measurement

frameworks should be proportionate to the severity of the NPL issues faced by the

bank.

Finally, given that the important role of efficient addressing of pre-arrears is a key

driver for the reduction of NPL inflows, a strong commitment of relevant staff

regarding the addressing of early warnings should also be fostered through the

remuneration policy and incentives framework.

3.3.4 Technical resources

One of the key success factors for the successful implementation of any NPL

strategy option is an adequate technical infrastructure. In this context, it is important

that all NPL-related data is centrally stored in robust and secured IT systems. Data

should be complete and up-to-date throughout the NPL workout process.

An adequate technical infrastructure should enable NPL WUs to:

• Easily access all relevant data and documentation including:

• current NPL and early arrears borrower information including automated

notifications in the case of updates;

• exposure and collateral/guarantee information linked to the borrower or

connected clients;

• monitoring/documentation tools with the IT capabilities to track

forbearance performance and effectiveness;

• status of workout activities and borrower interaction as well as details on

forbearance measures agreed etc.;

• foreclosed assets (where relevant);

• tracked cash flows of the loan and collateral;

Guidance to banks on non-performing loans − NPL governance and operations

26

• sources of underlying information and complete underlying documentation;

• access to central credit registers, land registers and other relevant external

data sources where technically possible.

• Efficiently process and monitor NPL workout activities including:

• automated workflows throughout the entire NPL life cycle;

• automated monitoring process (“tracking system”) for the loan status

ensuring a correct flagging of non-performing and forborne exposures;

• industrialised borrower communication approaches, e.g. through call

centres (including integrated card payment system software on all agent

desktops) or internet (e.g. file sharing system);

• incorporated early warning signals (see also section 3.5);

• automated reporting throughout the NPL workout lifecycle for NPL WU

management, the management body and other relevant managers as well

as the regulator;

• performance analysis of workout activities by NPL WU, sub-team and

expert (e.g. cure/success rate, rollover information, effectiveness of

restructuring options offered, cash collection rate, vintage analysis of cure

rates, promises kept rate at call centre, etc.);

• evolution monitoring of portfolio(s) / sub-portfolio(s) / cohorts / individual

borrowers.

• Define, analyse and measure NPLs and related borrowers:

• recognise NPLs and measure impairments;

• perform suitable NPL segmentation analysis and store outcomes for each

borrower;

• support the assessment of the borrower’s personal data, financial position

and repayment ability (borrower affordability assessment), at least for non-

complex borrowers;

• conduct calculations of (i) the net present value and (ii) the impact on the

capital position of the bank for each restructuring option and/or any likely

restructuring plan under any relevant legislation (e.g. foreclosures law,

insolvency laws) for each borrower.

The adequacy of technical infrastructure, including data quality, should be assessed

by an independent function on a regular basis (for instance internal or external

audit).

Guidance to banks on non-performing loans − NPL governance and operations

27

3.4 Control framework

Banks, especially high NPL banks, should implement effective and efficient control

processes for the NPL workout framework, in order to ensure full alignment between

the NPL strategy and operational plan on the one hand, and the bank’s overall

business strategy (including NPL strategy and operational plan) and risk appetite on

the other hand. Where these controls detect weaknesses, procedures should be in

place in order to address them in a timely and effective manner.

The control framework should involve all three lines of defence. The roles of the

different functions involved should be assigned and documented clearly to avoid

gaps or overlaps. Key outcomes of second and third-line activities as well as defined

mitigating actions and progress on those needs should be reported to the

management body regularly.

3.4.1 First line of defence controls

The first line of defence comprises control mechanisms within the operational units

that actually own and manage the bank’s risks in the specific NPL workout context,

mainly the NPL WUs (depending on the NPL operating model). Owners of first-line

controls are the managers of the operational units.

The key tools of first-line controls are adequate internal policies on the NPL workout

framework and a strong embeddedness of those policies in daily processes.

Therefore, the policy content should be incorporated into IT procedures, as much as

possible down to transaction level. Please see Annex 5 for key elements of NPL

framework-related policies that should be implemented at high NPL banks.

3.4.2 Second line of defence controls

Second line of defence functions are established to ensure on a continuous basis

that the first line of defence is operating as intended and usually comprises risk

control, compliance and other quality assurance functions. To adequately perform

their control tasks, second-line functions require a strong degree of independence

from functions performing business activities, including the NPL WUs.

The degree of control of the NPL framework by the second line should be

proportionate to the risk posed by NPLs and should place a special focus on:

1. monitoring and quantification of NPL-related risks on a granular and aggregate

basis, including linkage to internal/regulatory capital adequacy;

2. reviewing the performance of the overall NPL operating model as well as

elements of it (e.g. NPL WUs management/staff, outsourcing/servicing

arrangements, early warning mechanisms);

Guidance to banks on non-performing loans − NPL governance and operations

28

3. assuring quality throughout NPL loan processing, monitoring/ reporting (internal

and external), forbearance, provisioning, collateral valuation and NPL reporting;

in order to fulfil this role, a second-line function should have sufficient power to

intervene ex ante on the implementation of individual workout solutions

(including forbearance) or provisions;

4. reviewing alignment of NPL-related processes with internal policy and public

guidance, most notably related to NPL classifications, provisioning, collateral

valuations, forbearance and early warning mechanisms.

Risk control and compliance functions should also provide strong guidance in the

process of designing and reviewing NPL-related policies, especially with a view to

incorporating best practices to address issues identified in the past. At the very

minimum these functions should review the policies before they are approved by the

management body.

As indicated, the second-line controls constitute continuous activities. As an

example, for the early warning mechanism the following activities should be

performed at high NPL banks at a minimum on a quarterly basis:

• review the status of early warning indications and actions taken upon them;

• ensure that actions taken are in line with internal policies with regard to

timelines and types of actions;

• review adequacy and accuracy of early warning reporting;

• check whether the early warning indicators (EWIs) are effective, i.e. to what

extent have NPLs been detected (or not) at an early stage – feedback should

be provided directly to the respective function owning the early warning/watch-

list process; progress on methodology improvements should be tracked

subsequently (at least semi-annually).

3.4.3 Third line of defence controls

The third line of defence usually comprises the internal audit function. It should be

fully independent of functions performing business activities and, for high NPL

banks, it should have sufficient NPL workout expertise in order to perform its periodic

control activities on the efficiency and effectiveness of the NPL framework (including

first and second-line controls).

With regard to the NPL framework, the internal audit function should at least perform

regular assessments to verify adherence to internal NPL-related policies (see Annex

5) as well as to this guidance. This should also include random and unannounced

inspections and file reviews.

In determining the frequency, scope and scale of the controls to be carried out, a

proportionality approach should be taken into account. However, for high NPL banks

most of the policy/guidance compliance checks should be completed at least

Guidance to banks on non-performing loans − NPL governance and operations

29

annually and more frequently if significant irregularities and weaknesses have been

identified by recent audits.

Based on the results of its controls, the internal audit function should make

recommendations to the management body, bringing possible improvements to their

attention.

3.5 Monitoring of NPLs and NPL workout activities

The monitoring systems should be based on NPL targets approved in the NPL

strategy and related operational plans which are subsequently cascaded down to the

operational targets of the NPL WUs. A related framework of key performance

indicators (KPIs) should be developed to allow the management body and other

relevant managers to measure progress.

Clear processes should be established to ensure that the outcomes of the monitoring

of NPL indicators have an adequate and timely link to related business activities

such as pricing of credit risk and provisioning.

NPL-related KPIs can be grouped into several high-level categories, including but

not necessarily limited to:

1. high-level NPL metrics;

2. customer engagement and cash collection;

3. forbearance activities;

4. liquidation activities;

5. other (e.g. NPL-related profit and loss (P&L) items, foreclosed assets, early

warning indicators, outsourcing activities).

Further explanations of the individual categories are given below. High NPL banks

should define adequate indicators comparable with those listed below (see also the

summary benchmark in Annex 3), which are monitored on a periodic basis.

3.5.1 High-level NPL metrics

NPL ratio and coverage

Banks should closely monitor the relative and absolute levels of NPLs and early

arrears in their books at a sufficient level of portfolio granularity. Absolute and

relative levels of foreclosed assets (or other assets stemming from NPL activities),

as well as the levels of performing forborne exposures, should also be monitored.

Guidance to banks on non-performing loans − NPL governance and operations

30

Another key monitoring element is the level of impairment/provisions and

collateral/guarantees overall and for different NPL cohorts. These cohorts should be

defined using criteria which are relevant for the coverage levels in order to provide

the management body and other relevant managers with meaningful information

(e.g. by number of years since NPL classification, type of product/loan including

secured/unsecured, type of collateral and guarantees, country and region of

exposure, time to recovery and the use of the going and gone concern approach).

Coverage movements should also be monitored and reductions clearly explained in

the monitoring reports. The Texas ratio provides a link between NPL exposures and

capital levels and is therefore another useful KPI.

Where possible, indicators related to the NPL ratio/level and coverage should also

be appropriately benchmarked against peers in order to provide the management

body with a clear picture on competitive positioning and potential high-level

shortcomings.

Finally, banks should monitor their loss budget and its comparison with actual. This

should be sufficiently granular for the management body and other relevant

managers to understand the drivers of significant deviations from the plan.

NPL flows, default rates, migration rates and probabilities of default

Key figures on NPL inflows and outflows should be contained in periodic reporting to

the management body, including moves from/to NPLs, NPLs in probation,

performing, performing forborne and early arrears (≤90 dpd).

Inflows from a performing status to a non-performing status appear gradually (e.g.

from 0 dpd to 30dpd, 30dpd to 60dpd, 60dpd to 90dpd, etc.) but can also appear

suddenly (e.g. event driven). A useful monitoring tool for this area is the

establishment of migration matrices, which will track the flow of exposures into and

out of non-performing classification.

Banks should estimate the migration rates and the quality of the performing book

month by month, so that actions can be taken promptly (i.e. prioritise the actions) to

inhibit the deterioration of portfolio quality. Migration matrices can be further

elaborated by loan type (housing, consumer, real estate), by business unit or by

other relevant portfolio segment (see section 3.3.2) to identify whether the driver of

the flows is attributed to a specific loan segment.

24

3.5.2 Customer engagement and cash collection

Once NPL WUs have been established, key operational performance metrics should

be implemented to assess the unit or employees’ (if adequate) efficiency relative to

24

Constructing adequate historical time series of migration rates allows the calculation of annual default

rates which can feed the risk control department’s various models in estimating the probabilities of

default used for impairment review and stress testing exercises.

Guidance to banks on non-performing loans − NPL governance and operations

31

the average performance and/or standard benchmark indicators (if they exist). These

key operational measures should include both activity-type measures and efficiency-

type measures. The list below is indicative of the type of measures, without being

exhaustive:

• scheduled vs. actual borrower engagements;

• percentage of engagements converted to a payment or promise to pay;

• cash collected in absolute terms and cash collected vs. contractual cash

obligation split by:

• cash collected from customer payments;

• cash collected from other sources (e.g. collateral sale, salary

garnishments, bankruptcy proceedings);

• promises to pay secured and promises to pay kept vs. promises to pay due;

• total and long-term forbearance solutions agreed with the borrower (count and

volume).

3.5.3 Forbearance activities

One key tool available to banks to resolve or limit the impact of NPLs is

forbearance

25

, if properly managed. Banks should monitor forbearance activity in two

ways: efficiency and effectiveness. Efficiency relates mainly to the volume of credit

facilities offered forbearance and the time needed to negotiate with the borrower

while effectiveness relates to the degree of success of the forbearance option (i.e.

whether the revised/modified contractual obligations of the borrower are met).

In additional, proper monitoring of the quality of the forbearance is needed to ensure

that the ultimate outcome of the forbearance measures is the repayment of the

amount due and not a delaying of the assessment that the exposure is uncollectable.

In this regard, the type of solutions agreed should be monitored and long-term

(sustainable structural) solutions

26

should be separated from short-term (temporary)

solutions.

It is noted that modification in the terms and conditions of an exposure or refinancing

could take place in all phases of the credit life cycle; therefore, banks should ensure

that they monitor the forbearance activity of both performing and non-performing

exposures.

25

See section 5.3.1 for definition of forbearance.

26

See also chapter 4 regarding viable forbearance solutions.

Guidance to banks on non-performing loans − NPL governance and operations

32

Efficiency of forbearance activity

Depending on the potential targets set by the bank and the portfolio segmentation,

key metrics to measure their efficiency could be:

• the volume of concluded evaluations (both in number and value) submitted to

the authorised approval body for a defined time period;

• the volume of agreed modified solutions (both in number and value) reached

with the borrower for a defined time period;

• the value and number of positions resolved over a defined time period (in

absolute values and as a percentage of the initial stock).

It might also be useful to monitor the efficiency of other individual steps within the

workout process, e.g. length of decision-taking/approval procedure.

Effectiveness of forbearance activity

The ultimate target of loan modifications is to ensure that the modified contractual

obligations of the borrower are met and the solution found is viable (see also

chapter 4). In this respect, the type of agreed solutions per portfolio with similar

characteristics should be separated and the success rate of each solution should be

monitored over time.

Key metrics to monitor the success rate of each restructuring solution include:

• Forbearance cure rate and re-default rate: Given the fact that most of the

loans will present no evidence of financial difficulties right after the modification,

a cure period is needed to determine whether the loan has been effectively

cured.

27

The minimum cure period applied to determine cure rates should be

12 months aligned with the minimum cure period defined in the “EBA

Implementing Technical Standards (ITS) on supervisory reporting”

28

. Thus,

banks should conduct a vintage analysis and monitor the behaviour of forborne

credit facilities after 12 months from the date of modification to determine the

cure rate. This analysis should be conducted per loan segment (borrower with

similar characteristics) and, potentially, the extent of financial difficulties prior to

forbearance.

Cure of arrears on facilities presenting arrears could take place either through

forbearance measures of the credit facility (forborne cure) or naturally without

modification of the original terms of the credit facility (natural cure). Banks

should have a mechanism in place to monitor the rate and the volume of those

defaulted credit facilities cured naturally. The re-default rate is another key

27