2022

-

2023 Theatrical Season Report

Annual Analysis of Employment, Earnings, Membership and Finance

Russell Lehrer, Researcher

3

Is theatre in crisis? Is our industry in recovery? Over the last several months, I’ve heard these

questions asked over and over again. Both reveal the anxiety that many in our industry are

feeling at the end of the second full season to take place since the COVID-19 pandemic

shutdown. And as long as we continue to measure time by our distance from shutdown and

reopening, both questions will remain relevant.

Some sectors of our industry have returned more quickly and more robustly than others. But

for those stage managers and actors who haven’t yet returned to their pre-pandemic level of

employment, seeing others’ success may be cold comfort. And that goes double for those who

had not yet reached the level of employment they hoped for prior to the shutdown. Employers

who are laying o sta and tightening budgets are unlikely to feel relieved seeing their

colleagues at other theaters operating in full force.

But as you’ll read in the pages to come, by many of our benchmarks, the union’s numbers are

approaching – or in some cases, exceeding – some of our best seasons on record. It’s my hope

that this report will calm some of our worries, even if it doesn’t quite answer all of our questions.

We can feel encouraged by the positive trajectory this report describes, but let’s not celebrate

quite yet. ere is still work to be done to shape our industry into one that provides opportunity

to all its workers for a sustainable, middle-class life. But if there’s one message the labor

movement has for us and the world, it’s that together we can make that happen.

In solidarity,

Al Vincent, Jr.

FROM THE EXECUTIVE DIRECTOR

4

Coming out of an industry-wide shutdown, many of us – myself included – still view the

world through that lens. After years of consistently disappointing news, it can be jarring to

see evidence of a return to normalcy. And it is right and necessary to compare our individual

experiences to those of the union membership as a whole and the industry overall.

is report tells your stories. Every data point in this report is connected to an individual

member like you – the auditions or interviews you attended, the salary you were able to

negotiate and the work you performed backstage and on stage, as well as the contract terms only

achievable through your combined strength.

is report is a collective view of those individual experiences, one which shows remarkable

resilience. By every metric discussed here, the 2022–23 season was the healthiest for our

membership since the shutdown. Refreshingly, in many instances they approached or even

exceeded the pre-shutdown records for the union. But in areas where recovery lags, members

continue to struggle, and Equity continues to ght for your employment opportunities and

earnings.

Russell Lehrer

INTRODUCTION

5

e theatrical season, as referenced throughout this report, runs from June to May of every year.

In the 2022–2023 season members generated 276,757 work weeks, earning $474,919,343 across

all our contracts. So, how does this season compare to the previous 10 seasons, and to what

degree has the industry recovered from the 2020 shutdown?

e last full season before the COVID-19 industry shutdown – the 2018–2019 season – saw

historic highs in both member earnings ($479,292,441) and work weeks (328,788). By these

two critical measures, the 2022-2023 season reects a robust economic recovery – earning

50% higher than 2021–2022 and 1.2% higher than the record earnings of 2018–2019 – with

employment lagging close behind – 41% more employment than 2021–2022, though still 16%

behind the record employment of 2018–2019.

A YEAR IN REVIEW

6

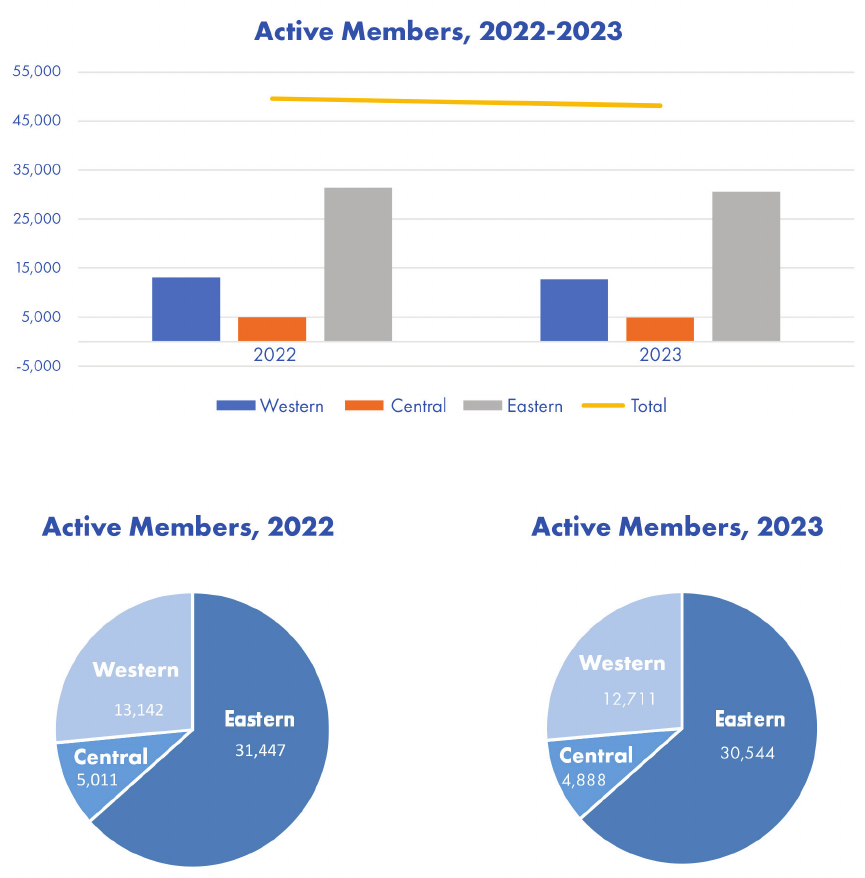

ere are many ways to quantify any union’s overall membership, and one of the most common

ways is active membership. Active membership includes members regardless of dues balance,

while not including members who have temporarily withdrawn from or formally suspended

payment of dues to the union. Looking at active membership by region for this season, the

geographic distribution of members in each region represents remained virtually unchanged

from last season, with the Eastern Region holding the largest share, followed by the Western

and Central Regions respectively. While these shares remain unchanged, there was a 2.9% drop

in total members from the previous season, down to 48,143 total active members as of June

2022, which aligned with the expiration of pandemic-era dues relief measures enacted by Equity.

7

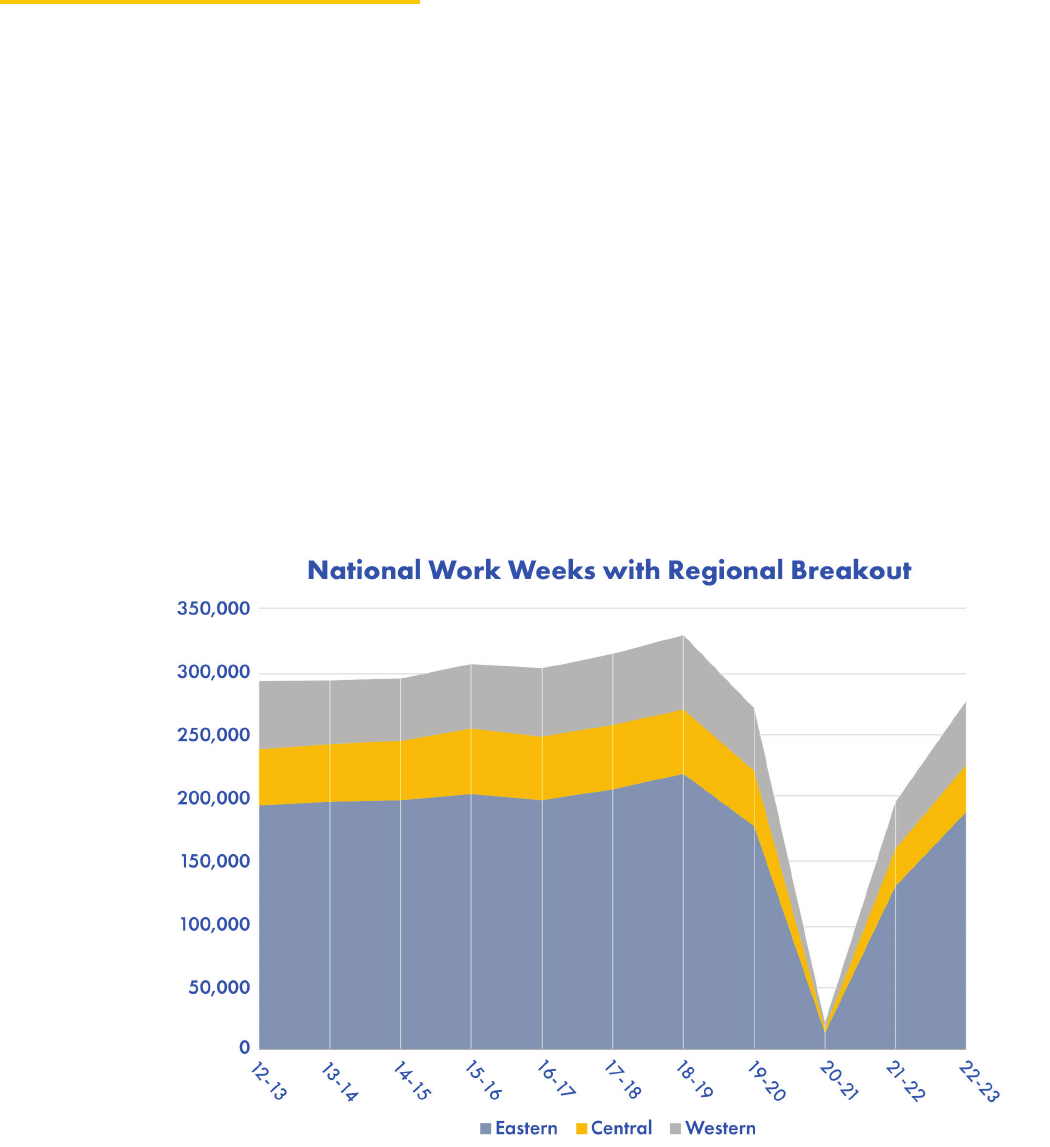

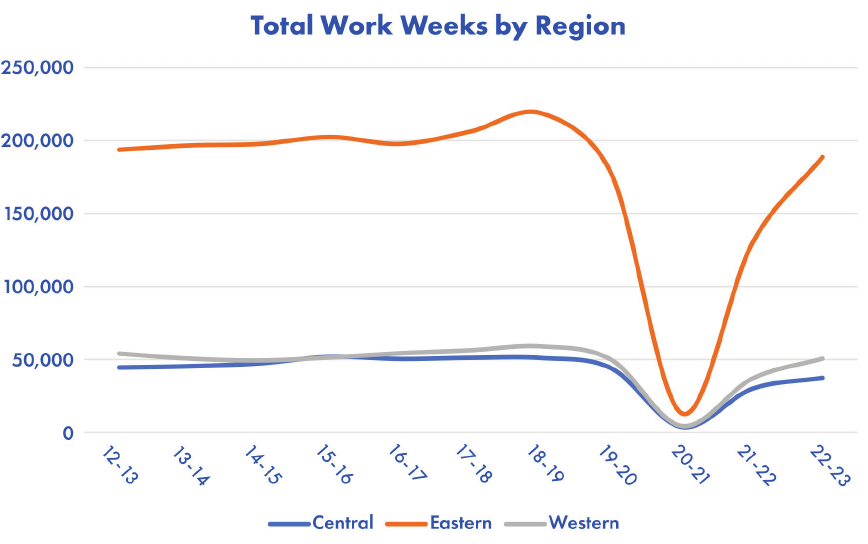

Work weeks are one of the key metrics that Actors’ Equity Association uses to analyze members’

employment. A work week is dened as a single week in which an individual member worked

for any amount of time. is allows us to account for the dierent lengths of individual member

contracts. A member does not need to work a whole week to have the work counted as a single

work week. e location and region associated with work weeks reects the location of the

employment, not the residence of the member employed.

ese rst two charts illustrate total work weeks, showing the combined regional work weeks

for the past 10 years and then each region’s work weeks broken out separately. is year we

continue the strong rebound from the loss of employment in the 2020–2021 season when

the industry shut down. e 2020–2021 season saw work week losses across all three regions

ranging between 91% and 93%. In this second season of recovery, regional work weeks increased

between 25% and 46% over the 2021–2022 levels.

WORK WEEKS

8

Looking rst to the Western Region, members worked a cumulative amount of 50,629 work

weeks, or 18.3% of all work weeks nationally. ese work weeks are an increase of 37.3% over

the 36,881 work weeks the previous season, while 14.2% below the record 2018–19 season.

In the Central Region, members worked a total of 37,422 work weeks, or 13.5% of all work

weeks this season. is is an increase of 25.1% over the 29,910 work weeks in 2021–22, and

73.3% of the work weeks earned in 2018–19.

Lastly, employment in the Eastern Region generated 188,706 work weeks, or 68.2% of all work

weeks. is is an increase of 45.6% above the 129,597 work weeks earned in the previous season,

though still 13.8% lower than the 2018–19 season.

Equity continues its eorts to ensure work week and employment opportunities increase for

the membership each year through a combination of organizing, contractual improvements and

industry health. We will see in the next section how member earnings oer another measure of

the theatrical season, and one with a sunnier outlook.

Many members seek work only as a stage manager, or only as a performer, and some performers

specialize in chorus work. is table shows work weeks for employment categories by nationally

and by region. Not only valuable in comparing work opportunities, this analysis is also critical

to Equity’s governance structure. Instead of the 10-year lookback we have employed elsewhere

in this report, we now focus only on the 6-year period referenced in Article 3, Section 2(c)

of Equity’s Constitution which denes how our National Council is composed, using these

statistics every 6 years.

9

Seasonal Work Weeks by Job Category and Region

National

Principal

Chorus

Stage Manager

Total

Central

Principal

Chorus

Stage Manager

Total

Eastern

Principal

Chorus

Stage Manager

Total

Western

Principal

Chorus

Stage Manager

Total

17-18

187,274

75,355

51,203

313,832

34,382

7,493

9, 319

51,194

112,573

62,084

31,673

206,330

40,319

5,778

10,211

56,308

18-19

195,910

77,455

55,423

328,788

33,061

8,108

9,901

51,070

121,038

63,073

34,649

218,760

41,811

6,274

10,873

58,958

19-20

163,504

61,418

45,638

270,560

29,243

6,145

8,487

43,875

99,399

49,706

27,898

177,003

34,862

5,567

9,253

49,682

20-21

13,496

2,109

4,379

19,984

2,538

12

846

3,396

7,880

1,959

2,393

12,232

3,078

138

1,140

4,356

21-22

113,604

39,737

33,968

187,309

20,349

2,456

5,661

28,466

69,010

33,497

20,757

123,264

24,245

3,784

7,550

35,579

22-23

176,204

57,154

43,399

276,757

27,843

3,004

6,575

37,422

112,213

48,828

27,665

188,706

36,148

5,322

9,159

50,629

Looking at the 2022–23 work weeks earned and again comparing them to the 2018–2019

season, we can take one measure of the industry’s return to its pre-pandemic heights. e chorus

work weeks nationally, for example, have not returned as robustly as either stage manager or

principal work weeks, with a particular lag in the Central Region.

National

Principal

Chorus

Stage Manager

Total

Central

Principal

Chorus

Stage Manager

Total

Eastern

Principal

Chorus

Stage Manager

Total

Western

Principal

Chorus

Stage Manager

Total

Work Weeks

89.9%

73.8%

78.3%

84.2%

84.2%

37.0%

66.4%

73.3%

92.7%

77.4%

80.0%

86.3%

86.5%

84.8%

84.2%

85.9%

2022-23 work

weeks as % of

18-19 work weeks

10

e following table provides a complete accounting of all work weeks from the 2022-23 season

by the underlying contractual agreement and region of employment.

Production

Point of Organization

Tours

Resident Theatre (LORT)

LORT Rep

LORT Non-Rep

Small Professional Theatre (SPT)

Letter of Agreement (LOA)

Short Engagement Touring (SETA)

Touring Agreement

Stock

COST

CORST

MSUA

RMTA

Developmental Agreement

Special Agreements

Theatre for Young Audiences (TYA)

Cabaret

Guest Artist

Special Appearance

University Theatre (URTA)

Dinner Theatre

Casino

Midsize

Business Theatre and Events

Staged Reading

Off-Broadway (NYC)

NYC-LOA

Mini (NYC)

Transition (NYC)

Showcase - LA

Showcase - NY

New England Area Theatre (NEAT)

Walt Disney World

Orlando Area Theatre (OAT)

Chicago Area (CAT)

Western Civic Light Opera (WCLO)

Hollywood Area (HAT)

San Francisco Bay Area (BAT)

Modified Bay Area Theatre (MBAT)

99 Seat Agreement

TOTAL

51,568

51,311

257

28,725

2,103

26,622

11,800

10,274

2,430

31,449

5,288

3,803

1,108

33

344

3,041

1,546

3,838

642

3,038

2,254

581

43

19

799

256

15,773

2,089

1,323

381

104

1,729

9,479

237

188,706

461

461

7,133

7,133

8,643

4,248

1,606

266

522

818

3,459

989

21

646

542

289

4,731

120

7

4,527

37,422

725

725

19,914

4,077

15,837

9,532

6,588

1,813

1,104

1,104

56

1,674

1,312

363

1,025

675

481

298

622

11

3

4

484

112

1, 319

197

2,317

50,629

52,754

52,497

257

55,772

6,180

49,592

29,975

21 ,11 0

2,430

33,262

7,998

5,173

1,630

851

344

3,097

6,679

6,139

1,026

4,709

3,471

1,351

5,072

622

19

930

266

15,773

2,089

1,323

381

4

104

1,729

9,479

237

4,527

484

112

1, 319

197

2,317

276,757

19.1%

19.0%

0.1%

20.2%

2.2%

17.9%

10.8%

7.6%

0.9%

12.0%

2.9%

1.9%

0.6%

0.3%

0.1%

1.1%

2.4%

2.2%

0.4%

1.7%

1.3%

0.5%

1.8%

0.2%

0.0%

0.3%

0.1%

5.7%

0.8%

0.5%

0.1%

0.0%

0.0%

0.6%

3.4%

0.1%

1.6%

0.2%

0.0%

0.5%

0.1%

0.8%

Eastern Central Western Total % of Total

11

Earnings, of course, are the other important factor in assessing a given theatrical season. Due

to collectively negotiated contractual increases as well as individually negotiated terms, earnings

are tied to but not merely a reection of work weeks. We will now examine the season along the

same frames of reference we have employed previously for work weeks taking member earnings

into account. e region to which earnings are attributed, as with work weeks, refers to the

region in which the employment occurred regardless of the member’s residence.

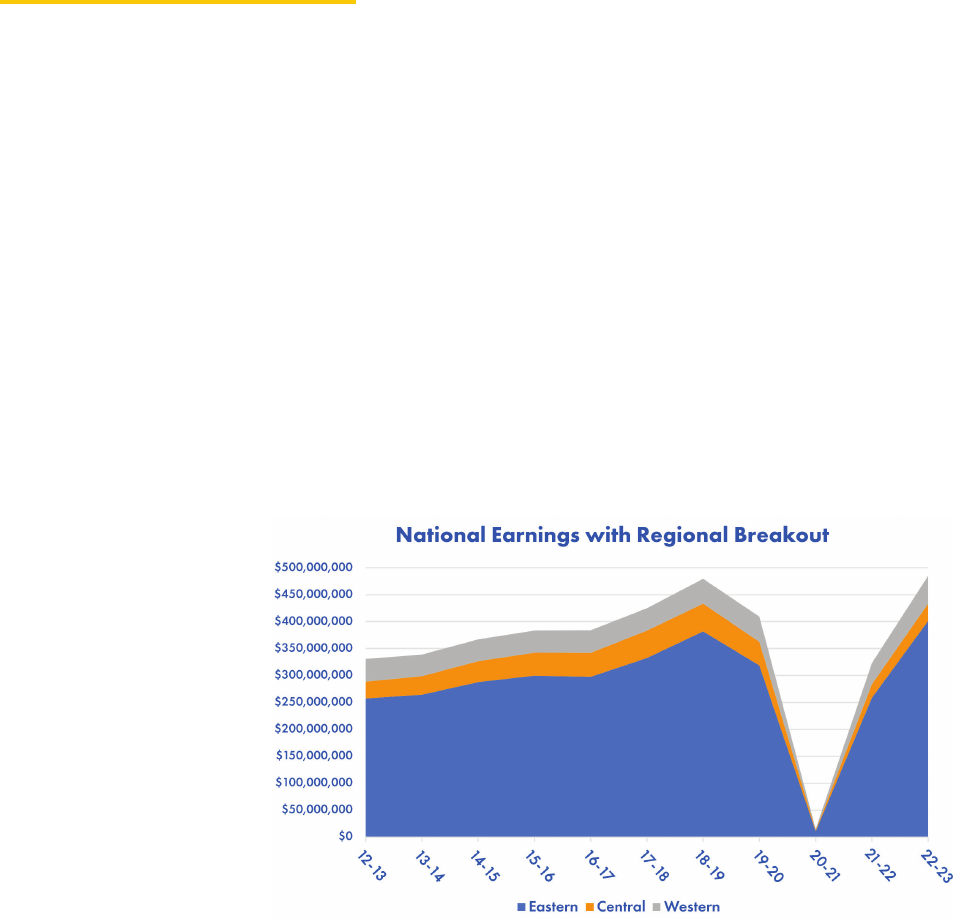

Again, we begin with charts illustrating national employment as earned in each of the regions

for the past 10 years, and then a regional breakout of these statistics. e nancial opportunities

aorded to our membership reect a more robust recovery than work weeks post-pandemic:

a full recovery nationally. Members earned $484,919,343 nationally in 2022–23, exceeding

the previous record earnings of 2018–19 ($479,292,411) by 1.2% while 2022–23 work weeks

remained at 84.2% of 2018–19 work weeks. National earnings increased by 50.1% in 2022–23

from earnings in 2021–22.

EARNINGS

Looking rst to the Western Region, members collectively earned $51,766,855, or 10.7% of

all earnings. ese earnings are an increase of 31.2% over the $39,351,903 earned the previous

season and are 12.1% higher than the 2018–19 season.

Shifting to the Central Region, members earned $31,763,162, which is 6.6% of all earnings this

season. While Central earnings continue to improve post-shutdown (up 25.1% from 2021–22),

the economic recovery lags behind the other regions. Central member earnings remain at 61.7%

of the record 2018–19 season.

12

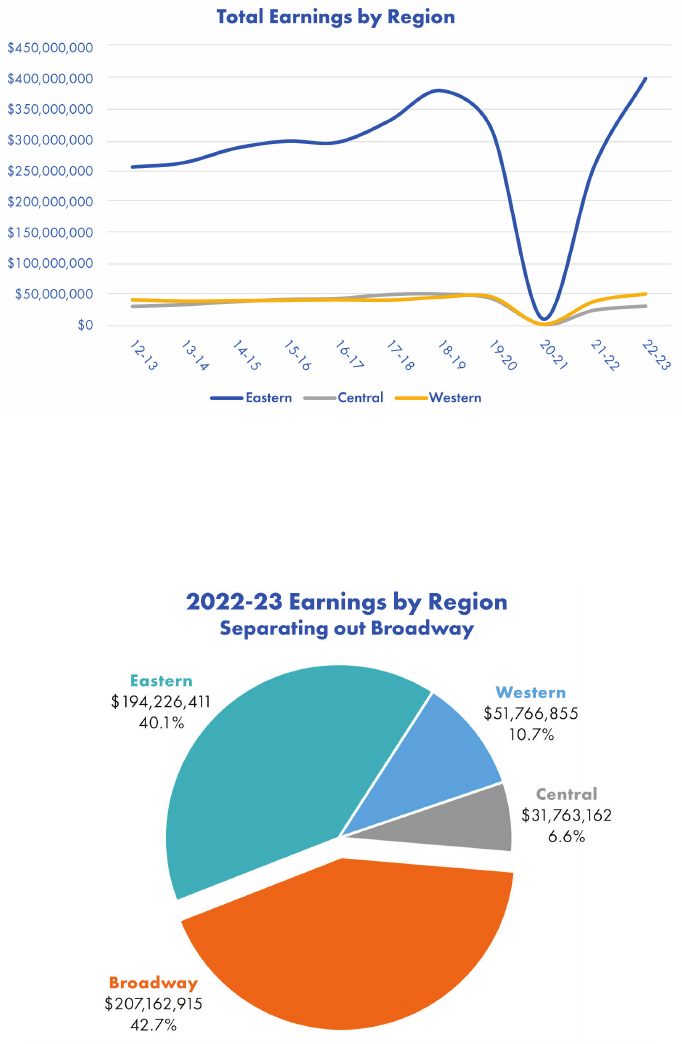

Lastly, the Eastern Region, including the income-leading Broadway employment, represented

82.8% of national member earnings, generating $401,389,326 this season. An increase of 55.2%

over 2021–22, these earnings are also 5.2% higher than 2018–19.

As noted previously, Broadway is an income leader to an outsized degree beyond its work weeks.

Broadway income alone represented 42.7% of the national earnings. But Broadway employment

alone does not account for the Eastern concentration of national nancial opportunities, as

illustrated in this graph. Of the $401,839,326 earned in the Eastern Region, $194,226,411

(48.3%) was earned in non-Broadway employment in 2022-23. Without Broadway earnings,

Eastern Region earnings were 3.7 times those in the Western Region, and 6.1 times those in the

Central Region (both other regions still counting any sit-down employment on the Production

Contract).

13

Production

Point of Organization

Tours

Resident Theatre (LORT)

LORT Rep

LORT Non-Rep

Small Professional Theatre (SPT)

Letter of Agreement (LOA)

Short Engagement Touring (SETA)

Touring Agreement

Stock

COST

CORST

MSUA

RMTA

Developmental Agreement

Special Agreements

Theatre for Young Audiences (TYA)

Cabaret

Guest Artist

Special Appearance

University Theatre (URTA)

Dinner Theatre

Casino

Midsize

Workshop

Business Theatre

Staged Reading

Royalties

Filming and Taping

Off-Broadway (NYC)

NYC-LOA

Mini (NYC)

Transition (NYC)

New England Area (NEAT)

Walt Disney World

Orlando Area (OAT)

Chicago Area (CAT)

Western Light Opera (WCLO)

Hollywood Area (HAT)

San Francisco Bay Area (BAT)

Modified Bay Area Theatre (MBAT)

99 Seat Agreement

TOTAL

Eastern

$252,305,851

$207,162,919

$45,142,933

$31,075,695

$1,895,409

$29,180,285

$7,573,427

$7,804,888

$18,964,342

$33,621,266

$5,648,072

$4,003,308

$974,531

$75,524

$594,709

$3,518,588

$1,784,761

$2,089,589

$609,531

$1,930,531

$991,380

$1,093,292

$25,683

$37,931

$21,488

$961,611

$2,365

$270,003

$21,822

$16,752,941

$1,438,402

$978,673

$197,260

$1,114,422

$10,441,915

$113,595

$401,389,326

82.77%

Central

$1,222,793

$1,222,793

$8,068,989

$8,068,989

$5,254,092

$3,662,551

$1,678,147

$337,180

$318,566

$1,022,401

$1,991,663

$623,620

$12,198

$390,026

$224,961

$335,918

$4,718,149

$120,000

$3,460,057

$31,763,162

6.55%

Western

$7,610,390

$7,610,390

$23,502,728

$5,151,548

$18,351,180

$5,454,158

$4,431,432

$2,087,941

$1,152,768

$1,152,768

$19,447

$1,694,051

$723,490

$301,225

$682,363

$254,004

$517,904

$178,734

$718,263

$6,600

$665,086

$72,880

$978,620

$77,746

$637,024

$51,766,855

10.68%

Total

$261,139,035

$215,996,102

$45,142,933

$62,647,412

$7,046,957

$55,600,455

$18,281,677

$15,898,871

$18,964,342

$35,709,207

$8,478,987

$5,493,256

$1,293,097

$1,097,925

$594,709

$3,538,036

$5,470,474

$3,436,700

$922,954

$3,002,920

$1,470,345

$1,947,115

$4,922,565

$718,263

$37,931

$21,488

$1,088,211

$2,365

$270,003

$21,822

$16,752,941

$1,438,402

$978,673

$197,260

$1,114,422

$10,441,915

$113,595

$3,460,057

$665,086

$72,880

$978,620

$77,746

$637,024

$484,919,343

% of Total

53.85%

44.54%

9.31%

12.92%

1.45%

11.47%

3.77%

3.28%

3.91%

7.36%

1.75%

1.13%

0.27%

0.23%

0.12%

0.73%

1.13%

0.71%

0.19%

0.62%

0.30%

0.40%

1.02%

0.15%

0.01%

0.00%

0.22%

0.00%

0.06%

0.00%

3.45%

0.30%

0.20%

0.04%

0.23%

2.15%

0.02%

0.71%

0.14%

0.02%

0.20%

0.02%

0.13%

e following table provides a complete accounting of all earnings from the 2022–23 season by

underlying contractual agreement and region of employment.

14

In this section we will look more closely at the three collectively bargained agreements which

each represent at least 10% of both annual work weeks and member earnings.

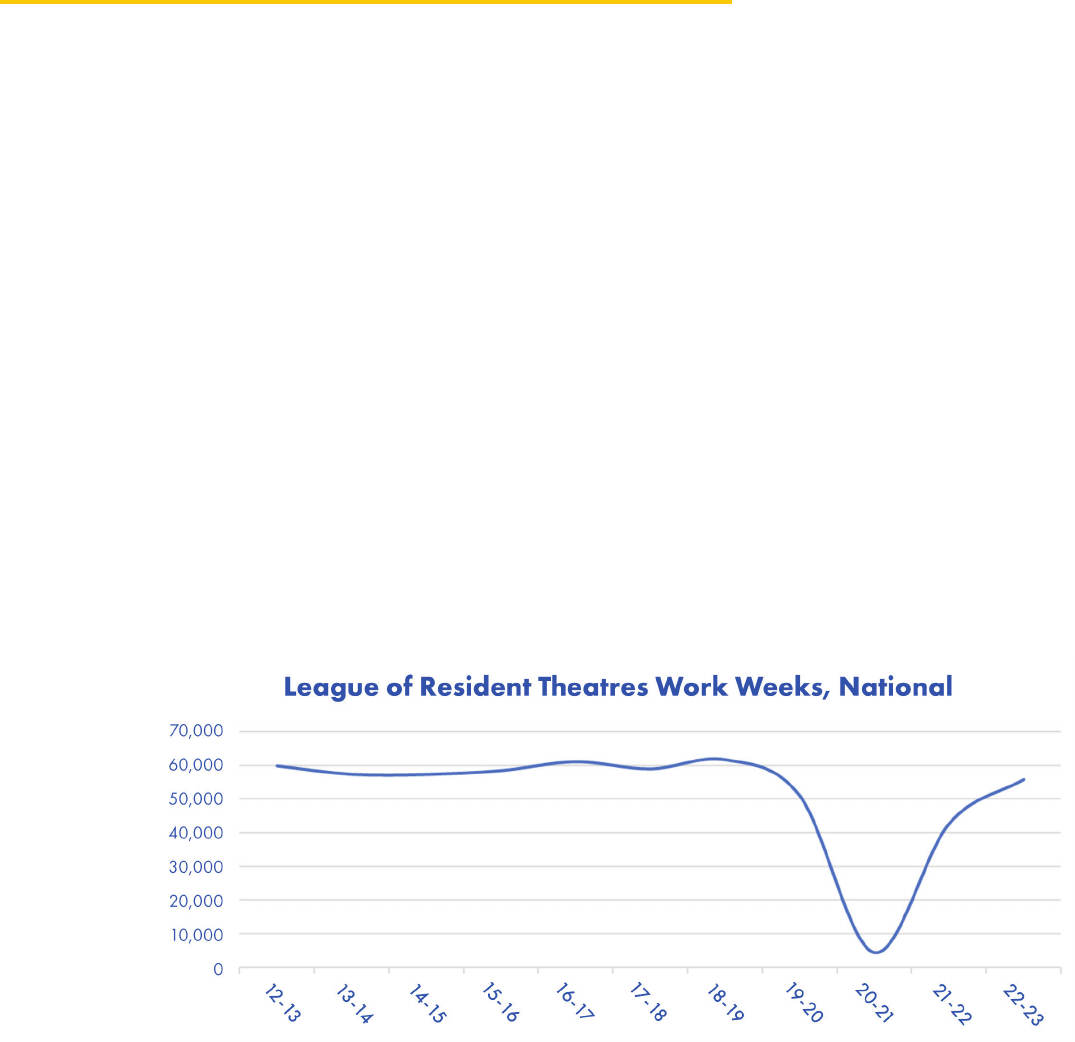

LORT

e League of Resident eatres (LORT) has 80 member theatres in 30 states and the District

of Columbia. Since 1965 the League of Resident eatres Agreement has consistently been one

of the largest generators of work weeks for members without being consigned to a single region.

During the 2022–23 season, a few LORT producers have made headlines with downsizing

eorts, seasonal hiatuses or unfortunate closures. Future seasons may reect declines in work

weeks or earnings, but such eects are not notable in the 2022–23 season. is theatrical

season, the LORT Agreement continued its post-pandemic recovery with 55,772 work weeks,

providing 20.2% of all national work weeks. at is a LORT-earned work week increase of

30.7% more work weeks than in 2021–22, to 90.5% of the work weeks in 2018–19. e Western

and Eastern Regions fared slightly better than the Central. Western LORT work weeks were

93.6% of their 2018–19 numbers while Eastern LORT work weeks were 91.0% and Central

LORT work weeks were 81.1% of their respective 2018–19 employment.

LORT, Touring, Production Details

15

Nationally, LORT employment provided $62,647,412 in member earnings, 99.8% of the 2018–

19 LORT earnings and 12.9% of all earnings in 2022-23.

16

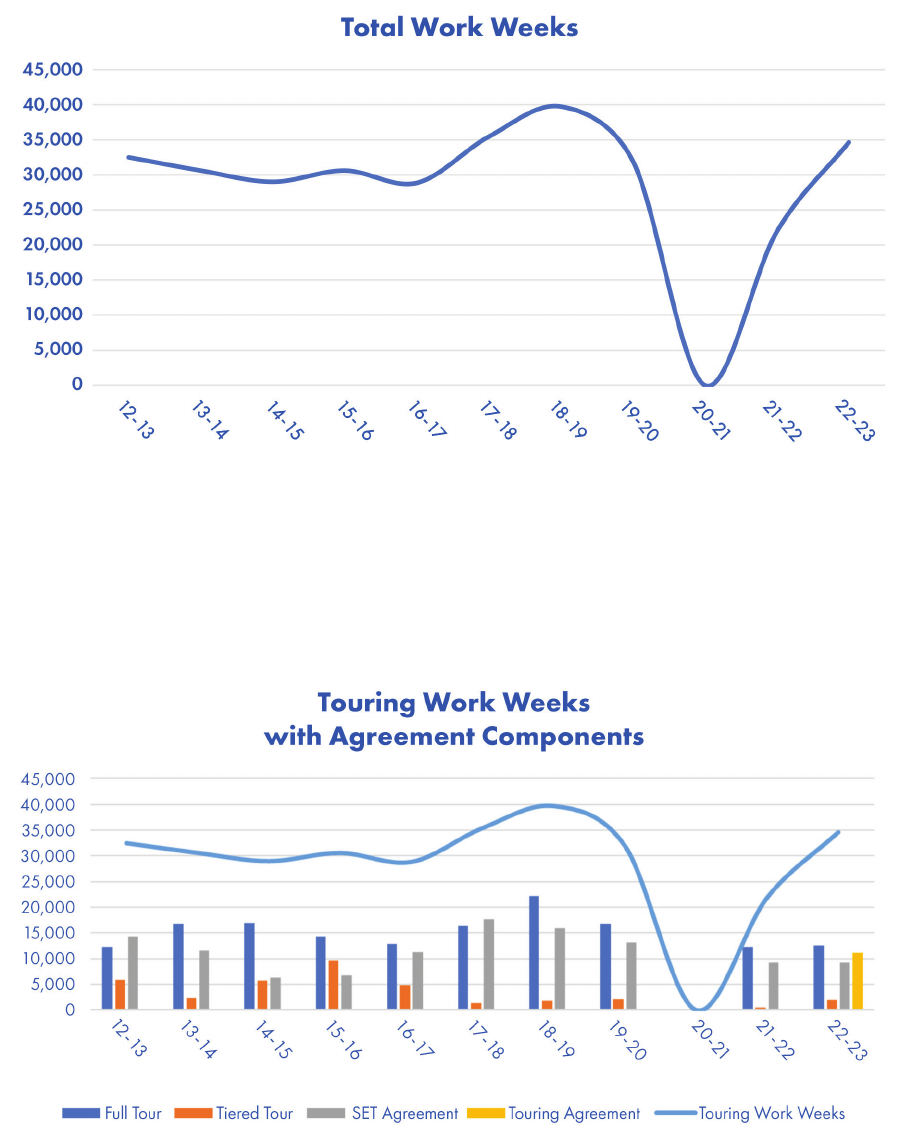

TOURING

Agreements covering national tours have their contractual origins in the Production Contract.

First negotiated in 1919, the Production Contract is the oldest agreement that Equity

collectively bargains and administers. Historically covering both sit-down productions (also

known as Point of Organization productions) including Broadway and tours (national and

tiered), during this season Equity negotiated a separate agreement for touring bringing together

national, tiered and short engagement touring. is contractual realignment was a long-sought

institutional goal and achieved many needed and deserved improvements for members touring

on both the Production Contract and the Short Engagement Touring Agreement (SETA). is

consolidation to a unied Touring Agreement does, however, provide a momentary statistical

challenge in providing seasonal gures and context for this annual report. For long-term analytic

reasons and contractual administration, the productions that were touring on the Monday

following the new agreement’s ratication (May 1, 2023) and continued touring on the new

Touring Agreement have been retroactively classied to the Touring Agreement to their rst

employment date in previous seasons, while those that had closed prior to ratication have

retained their historic classication.

To better contextualize the Production Contract statistics examined in the next section, with

touring removed for the rst time in Equity’s history, our analysis will start with Touring,

looking at all touring employment historically. In 2022–23, tours (including Tiered Tours) on

Production, SETA and the new Touring Agreement provided 34,627 work weeks, 87.2% of the

39,730 work weeks earned in 2018–19 on the then-existing touring agreements.

17

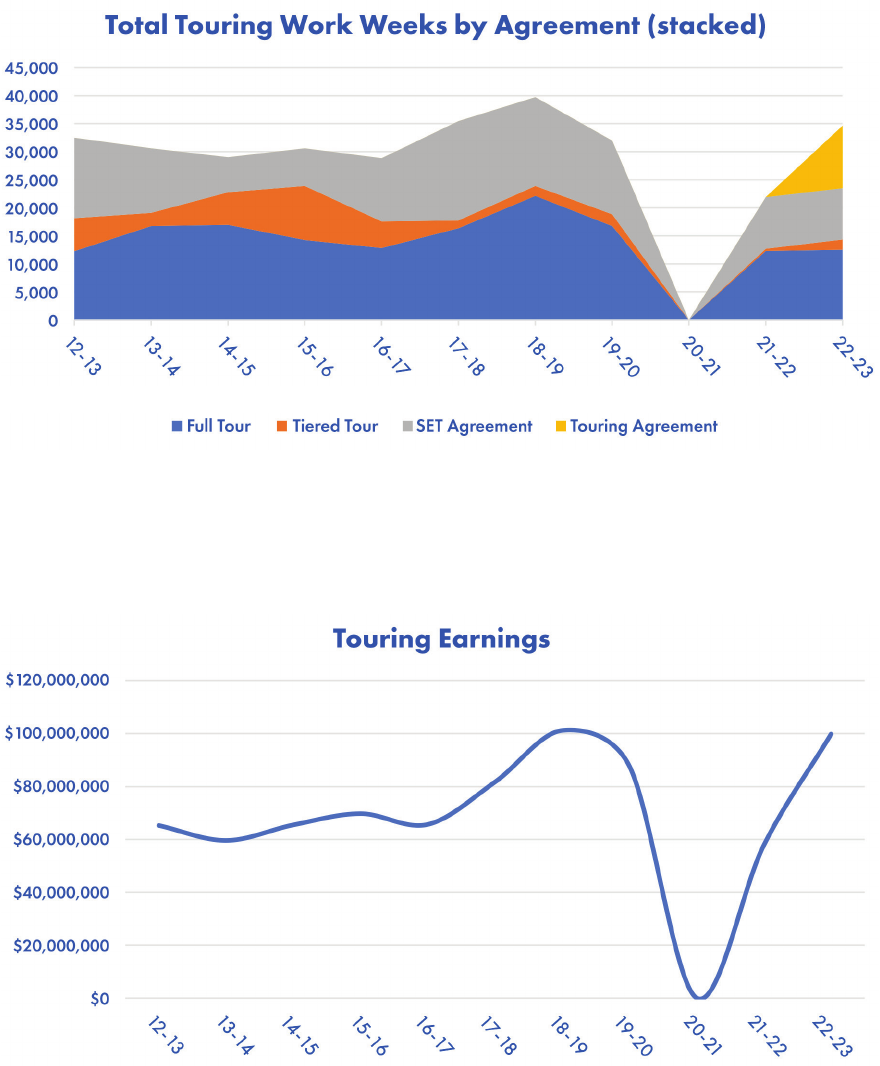

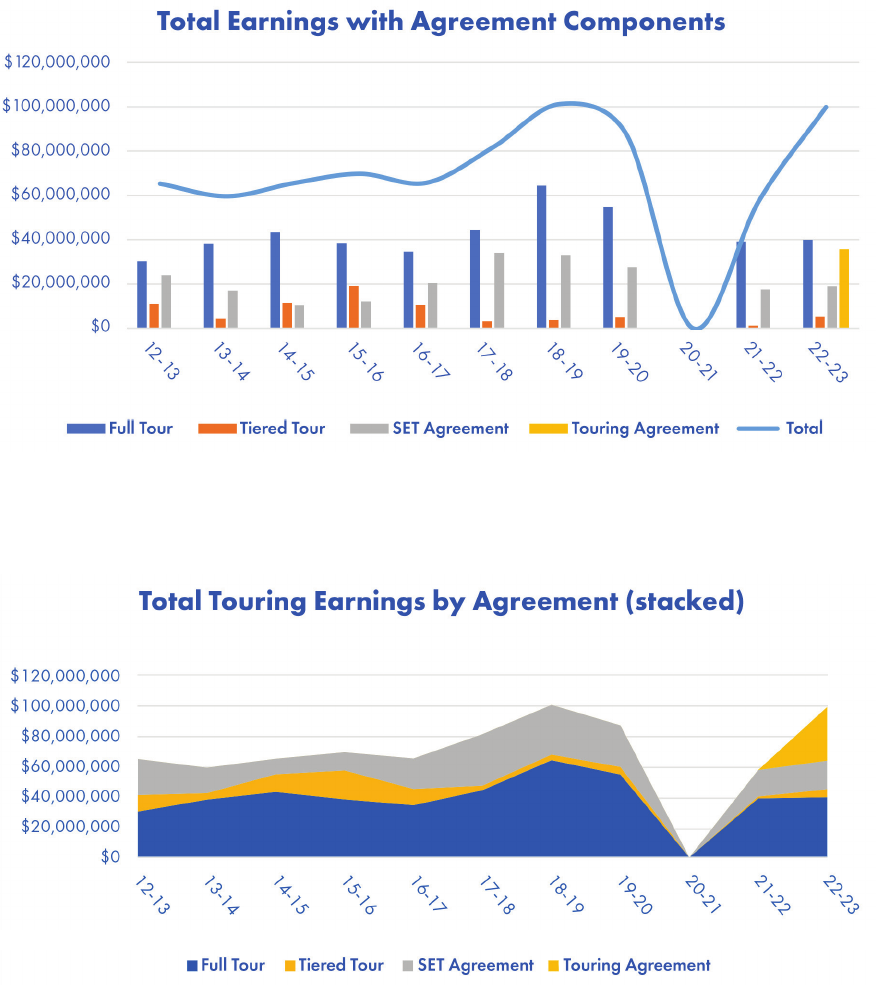

With the vast majority of tours now operating under the Touring Agreement, the following

chart shows the historic distribution and contribution to work weeks of each national touring

agreement.

18

Touring employment across three agreements earned members $99,816,480 in 2022–23, 98.6%

of the record $101,213,443 earned in 2018–19.

Looking at the component agreements, again please note that in the chart below historic

earnings are attributed to the agreement that was in place either at the tour’s conclusion or in

place as the tour continues after the new agreement was ratied. In subsequent annual reports,

all national touring employment will be categorized under the new contract, the Touring

Agreement.

19

20

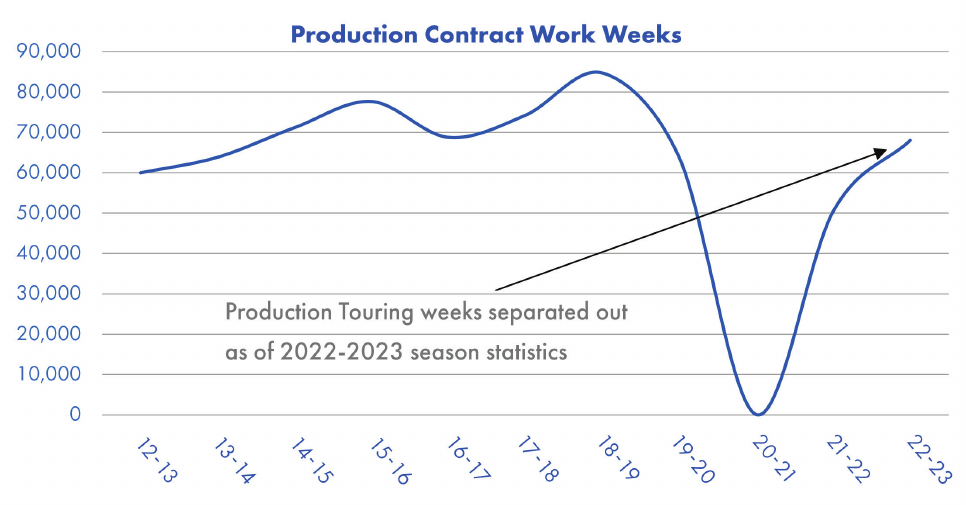

In order to look at the Production Contract in context, we can isolate the non-touring

employment on the agreement historically to the 2007–08 season. In previous reports,

non-touring employment on the Production Contract is denoted as Point of Organization

employment.

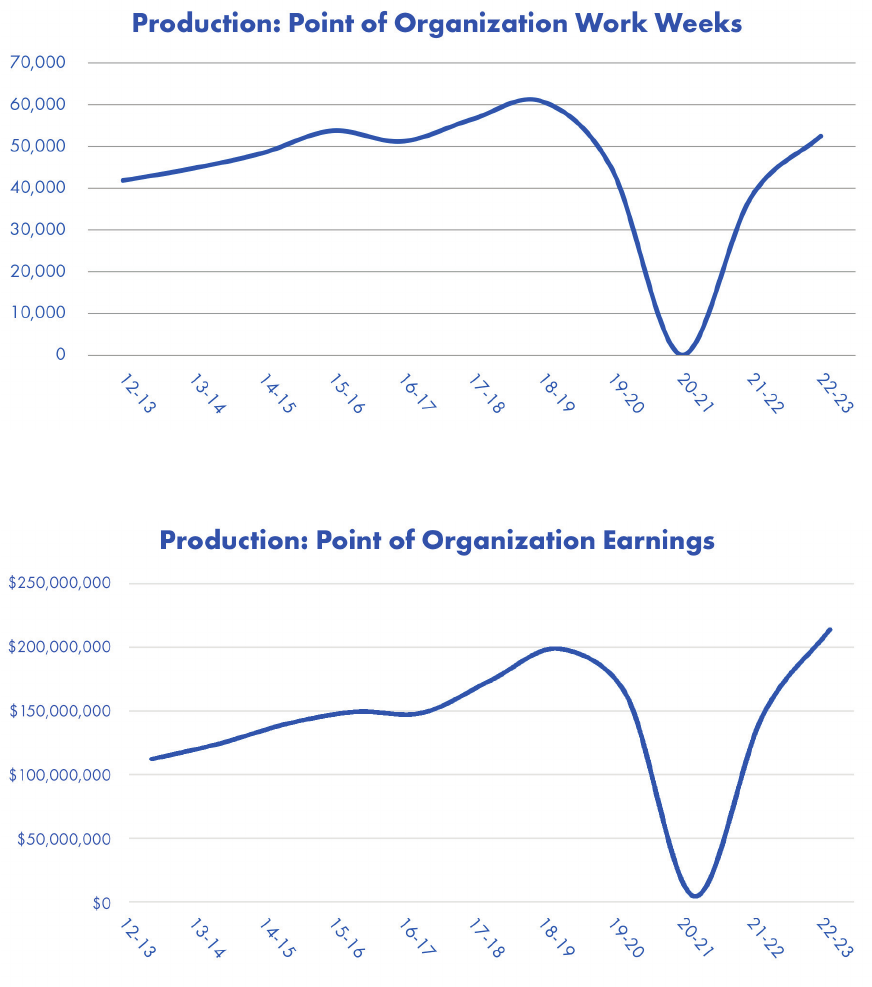

Nationally in 2022–23, members worked for 52,497 work weeks in sit-down Production

Contract employment. at’s a 38.9% increase over the previous season post-shut down, and a

return to 86.3% of the high mark set by the 2018–19 season. Earnings on these contracts again

tell a dierent story of recovery.

PRODUCTION

With this sizeable portion of touring employment that previously was on the Production

Contract reassigned to touring statistics, it is not surprising the following chart gives a

misperception of lost work on the Production Contract. is includes sit-down productions

outside of New York City as well as Broadway.

21

As a result of collectively bargained contractual increases and terms individually negotiated by

members, the 2022–23 earnings ($215,996,102) exceeded by 7.8% the earnings in 2018–2019

($200,456,656). e increase in earnings colors the impact of the slower return to pre-pandemic

employment.

22

Race or Ethnicity

Asian or Asian American

Black or African American

Hispanic or Latin American

Indigenous Hawaiian or Pacific Islander

Indigenous North American

Middle Eastern or North African

Multi-Racial or Multi-Ethnic

White or European American

Prefer Not To Say

Not Provided

National Total

%

Female

656

2,201

811

23

44

48

1,377

15,595

1,251

2,335

24,341

50.56%

Male

463

2,148

889

33

44

50

1,086

15,004

1,140

2,328

23,185

48.16%

8

36

22

1

62

194

13

8

344

0.71%

Non-Binary/

Third Gender

2

2

2

1

1

10

33

77

6

134

0.28%

Prefer Not

to Say

2

7

5

1

1

10

35

4

1

66

0.14%

Prefer to

Self-Describe

1

6

1

2

7

6

50

73

0.15%

Not

Provided

Total

1,132

4,400

1,730

56

90

101

2,547

30,868

2,491

4,728

48,143

%

2.35%

9.14%

3.59%

0.12%

0.19%

0.21%

5.29%

64.12%

5.17%

9.82%

e demographics in the table above are generated at the end of the season each year. is table

reects the active membership based on how members self-identify their gender and race or

ethnicity, information which the union maintains under strict condentiality. is report simply

looks at our membership at a specic point in time.

Even though we look at membership at a given moment in time above, Equity’s membership

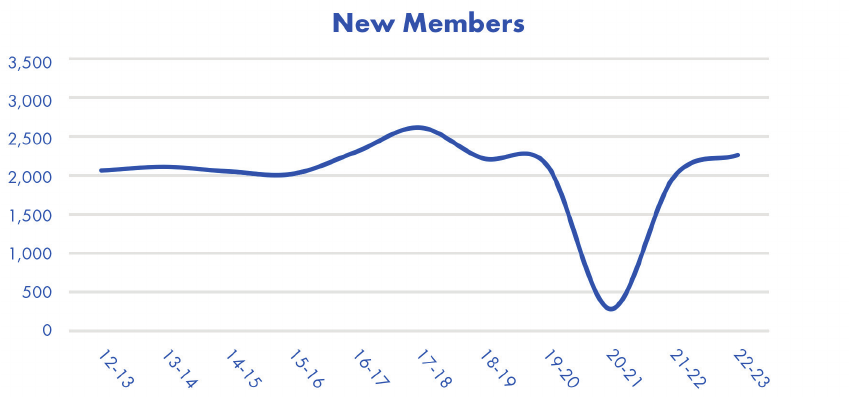

is not static. Between 1991 and 2019, Equity added an average of 2,302 new members each

theatrical season. In 2022–23, Equity added 2,303 new members, continuing to build on the

Open Access membership policy and newly organized work opportunities.

From the outward view of employment, we shift to the critical inward analysis of our

membership. Equity members provide not only the union’s strength but through their

participation in governance and negotiations they dene the union’s goals. A union is nothing

without its members, but who is Equity? Each year this report takes a moment to examine the

people that make up Equity’s membership, expanding on the regional gures discussed in the

Year In Review section of this report.

MEMBERSHIP

23

24

Up until this section, this report has analyzed data and shared statistics from the eatrical

Season which Equity has dened as June to May of the following year. However, for this section

we shift our focus to data that correlates to Equity’s scal year which runs from April to March

of the following year.

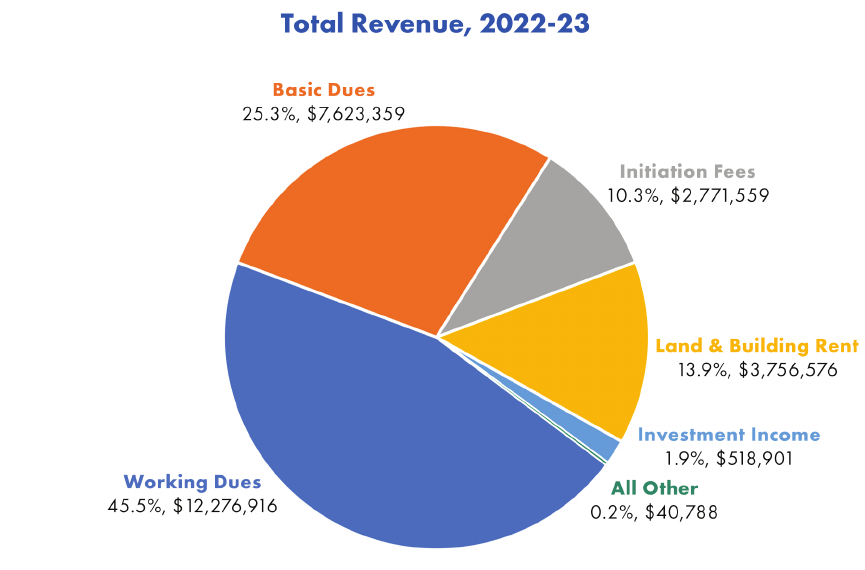

Equity has three categories of member-generated revenue: initiation fees, basic dues and

working dues. With the exception of the two years of industry shut down, this revenue accounts

for the majority of the funds which enable Equity to represent members and enforce its

collectively bargained agreements. e initiation fee is the initial payment made when a member

joins the union. is fee doesn’t have to be paid in one lump sum upfront and generally is paid

in installments when a member is working. Basic dues are collected from all members biannually

in the spring and fall. Collected when a member is working on an Equity contract, working dues

are calculated as a percentage of a member’s Equity-contracted income.

FINANCES (unaudited)

25

In addition to these three member-generated revenue streams, Equity has investments (both

nancial assets and real estate holdings) which account for 16.0% of Equity’s 2022–23 revenue.

Equity’s property-related revenue is generated by the land it owns in Times Square, New

York City, the building it owns in the West Loop, Chicago, and the building it owns in North

Hollywood, Los Angeles.

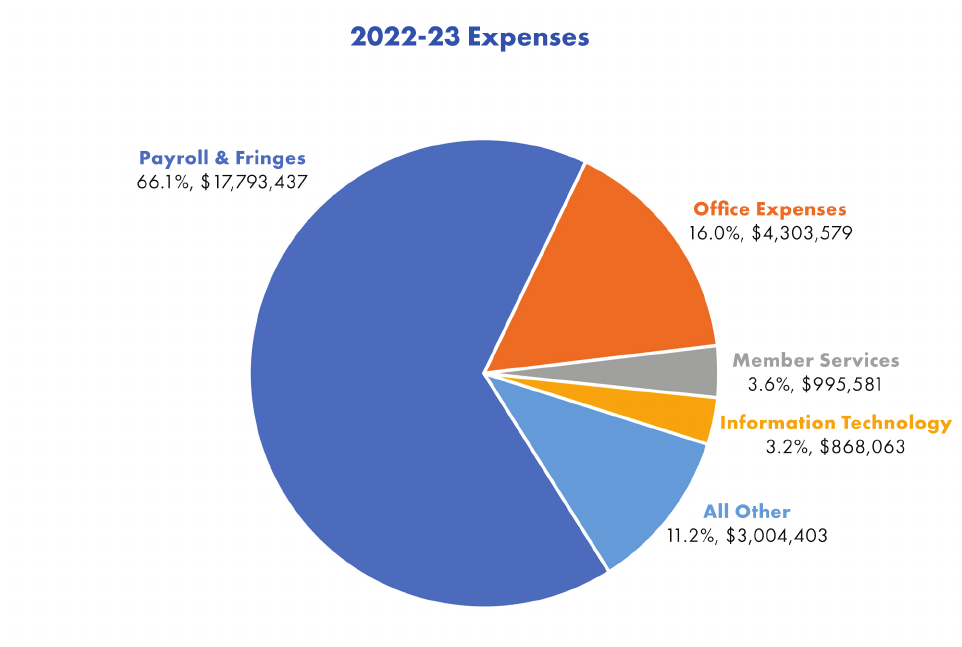

is nal chart illustrates Equity’s expenses. Most of Equity’s expenses go directly towards

maintaining member services:

• the dedicated sta that keeps the union running strong (payroll and

fringes);

• the oces and the information technology, including maintenance

with which they provide these services (oce expenses and information

technology);

• direct member services expenses, including all governance-related

expenses, contract negotiations and ratications;

• member communication and travel to worksites to inspect conditions,

meet directly with members and enforce contractual terms.

26

e industry shutdown in 2020 aected the union’s nances as well as those of its members.

As we look to all measures of our industry’s recovery, we conclude this nancial section of the

report noting that, following a period during which Equity’s council appropriated reserves

to maintain necessary member services, Equity was able to resume full operations while

maintaining nancial stability.

27

ere is great value in stepping back to assess the entire industry’s health from a distance,

be it a backward look to the most recent theatrical season or gathering context from further

back in the business’s history. But no matter what landscape we lay out, you should recognize

yourself as part of that scene. is report tells multiple stories, and they are all important. e

nancial health of Broadway has undeniable ripple eects for the rest of our union, but the lost

employment evidenced in the reduced work weeks and the lagging recovery elsewhere represent

actual members who are still suering from the pandemic’s eects on live theatre.

I see this report as adding another chapter to Equity’s long tradition of keeping both the

concerns of individual members and live theatre’s evolving needs at the heart of all its

decisions. If you’re an Equity member, this report is meant to provide a view of how the entire

membership is faring in this challenging recovery period, to add to what you know about how

you personally are faring. I hope you can bring your personal experiences seeking work and

in the workplace to color what’s shared here and to deepen your own understanding of the

industry. Together we can continue to make inroads for increased work opportunity, improve

working conditions, and to address your concerns for where live theater is headed.

is eatrical Season Report could not have been written alone, and it builds on the exemplary

work of previous authors Joey Stamp and Steve DiPaola. Assistant Executive Director for

Finance and Administration Regina Garlin and Controller Bryant Lee provided insight and

all data regarding Equity’s nances. None of the statistics on employment and earnings would

be possible without the diligent, daily eorts of the membership associates and the contract

membership associates overseen by Director of Membership John Fasulo and Director of

Contracts Katey Schwartz. e visual and textual assistance from Communications Director

David Levy, Designer Noah Diamond and Senior Writer and Project Manager Gabriela

Geselowitz were invaluable. And it is impossible to overstate the important contributions of

Director of Information Technology Doug Beebe, whose understanding of Equity’s workings

and its data is unsurpassed. Now in my third decade at Equity, it remains a privilege to work

alongside a sta dedicated to serving professional artists.

CURTAIN CALL